Trump Did It: Executives & Administrators Are Increasingly Using TDI To Fight DEI Authored by Jonathan Turley, “Trump made me...

Read More

Market Has Reached “Exhaustion Equilibrium”, Gamma-Hedging Flow Impacts Will Only Get Worse From Here

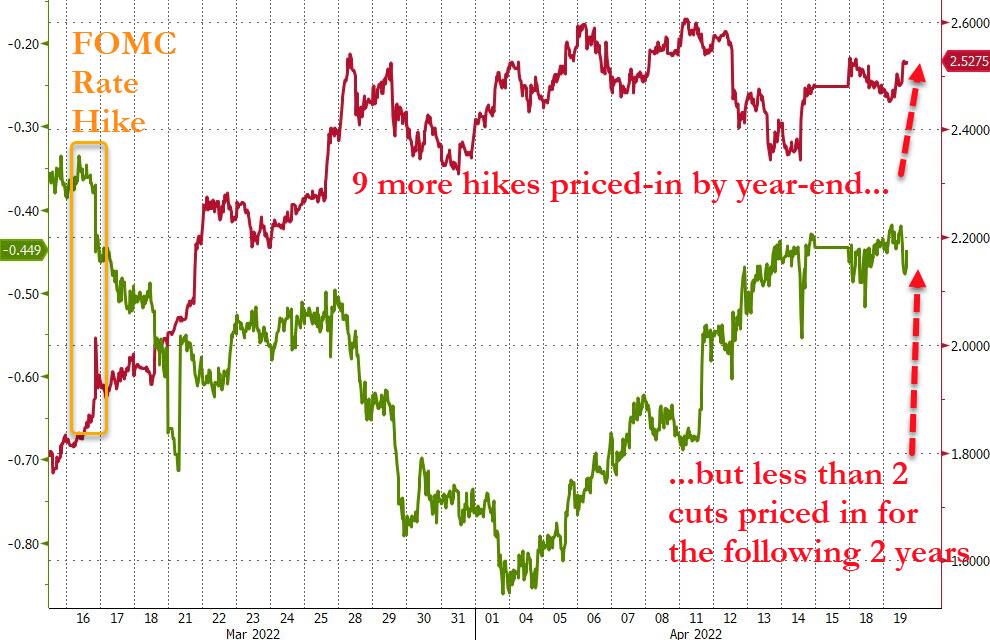

Stocks have shrugged off St.Louis Fed President Bullard’s “75bps” optionality comments (still not base case – but 50bps at each meeting in 2022 is) this morning, rampaging penny-stock-like back into the green since last Thursday’s close…

{kind=link}

As Nomura’s Charlie McElligott wrote in a note this morning, this is consistent with what we’ve been seeing and hearing from many who have grown outright numb and skeptical of further “hawkishness” catalysts from here, being viewed as at least locally “fully-priced” for now, after the recent CPI print gave a glimmer of hope to the “peak inflation is behind us” crowd.

{kind=link}

The Fed getting to “neutral” is a yawn now; from here, you’re gonna need to hear wide-spread FOMC advocacy of running RESTRICTIVE policy, requiring upgraded rhetoric from the Fed stating that they’d be willing to negatively impact Labor / Jobs in order to crush the inflation problem in any Bullard-style fashion, and see a pivot from market’s current pricing of tightening cycle “peak” in mid ’23 – and instead, see hikes added-back late ’23 into ’24 as opposed to the current Fed cuts that are priced there!

But, there’s something even more concerning lurking behind the scenes in markets. One look at the chaotic swings in yesterday and today’s cash trading sessions (top chart) brings to mind that fact that beginning yesterday, the CBOE began listing Tuesday SPX Weekly Options (4/26 and 5/3 expiries), with the first Thursday Weeklies scheduled for listing on 5/11 (5/26 and 5/29 expiries)… all of which means that in a month, SPX Options will expire EVERY. DAY. OF. THE. WEEK. (h/t Bill Luby @VIXandMore)

McElligott spells out what that means: “Gamma hedging flow impact is only going to get worse from here…”

This is ESPECIALLY the case due to the (embarrassingly) enormous popularity of short-dated options… over 50% of total SPX Options Volume is now btwn 0-5 days-to-expiration, with over 30% at 0 to 1DTE (!); and for SPY—aka “retail” size—it’s even worse: 0-5DTE options are over 70% of total volume, and 0-1DTE are ~50%

The trade into May’s big FOMC meeting feels “short Vol, short Delta” – but once we get that clarity and event-risk clearance, Bond stabilization likelihood grows, and will bring out more “structural buyers” which then too will see Equities likely firming into rest of year, enjoying their ride into the mid / late ’23 “Recession” sunset.

Additionally, SpotGamma flagged heavy negative delta trading yesterday in SPY/QQQ which has led to a +10-20% increase in negative gamma for those ETF’s. This implies higher rates of potential volatility.

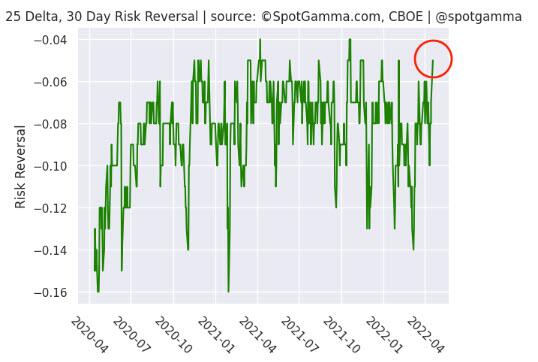

The market appears to be generally accepting these lower prices without much fear. This morning our risk reversal metric measures -0.05 which is typically a level associated with large bullish moves in equities. This indicates an increase in call options prices, despite call volumes (i.e. demand) not increasing. Our initial thought is that this is due to dealer pricing of FOMC meeting in early May. The other implication is that puts may be relatively cheap.

{kind=link}

Overall it seems that the market has reached something of an exhaustion equilibrium.

At this point traders have had the opportunity to price in both fiscal/monetary & geopolitical risks and sell accordingly. It’s also clear that the tail risk remains elevated, and that keeps the VIX elevated.

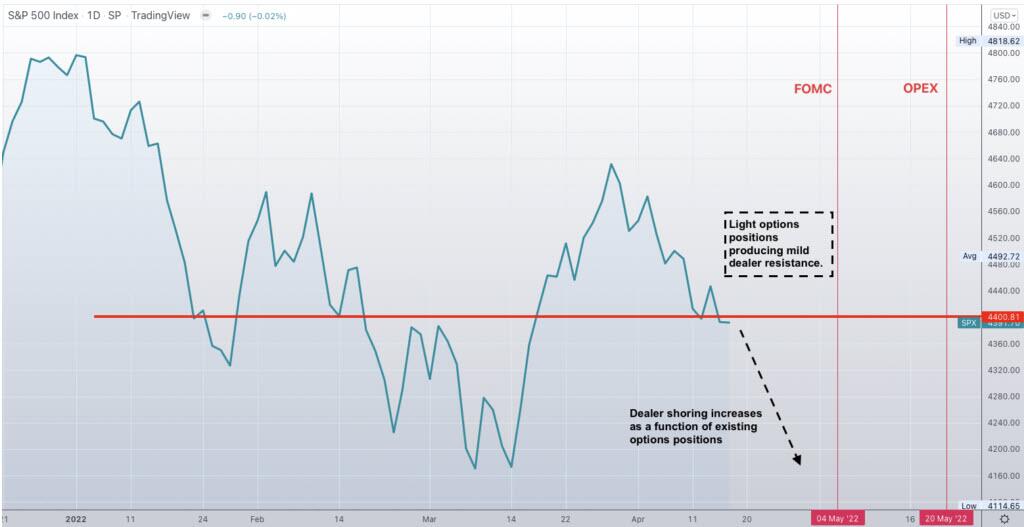

The issue for markets here is that if the S&P slides lower, it’s likely dealer shorting starts to increase incrementally.

{kind=link}

If a downside cycle initiates from here, it creates a reflexive feedback loop wherein dealers are selling which drives higher implied volatility and more downside demand.

{kind=link}

Further, the two events ahead that could break a cycle like this would be 5/4 (FOMC) and May OpEX (5/20).

Finally, for the dip-buyers, SpotGamma warns that risks to the upside continue to remain muted, as significant volatility selling likely cannot commence without clarity from the Fed and/or a resolution of geopolitical risks (i.e. a Russian/Ukraine ceasefire).

Tyler Durden

Tue, 04/19/2022 – 13:50

Please follow and like us: