A Third Of Americans Worry About Manipulated News Almost half of the people surveyed in the United States as part of a...

Read More

Netflix Monkeyhammered 20% Lower On Catastrophic Earnings, Sees Loss Of 2 Million Subs In Q2

Recent earnings reports from streaming giant Netflix had been a volatile rollerocaster: the stock tumbled just over one year ago when the company reported a huge miss in both EPS and new subs, which at 2.2 million was tied for the worst quarter in the past five years, while also reporting a worse than expected outlook for the current quarter. This reversed five quarters ago when Netflix reported a blowout subscriber beat and projected it would soon be cash flow positive, sending its stock soaring to an all time high – if only briefly before again reversing and then tumbling four quarters ago when Netflix again disappointed when it reported a huge subscriber miss and giving dismal guidance, leading to the second quarter when Netflix slumped again after the company missed estimates and guided lower. This again reversed two quarters ago when Netflix soared after it blew away expectations and guided to a blowout Q4, only to plummet last quarter when the company’s stock crashed after NFLX reported a dismal subscriber miss for Q4 and gave horrific guidance for the current quarter.

{kind=link}

Heading into today’s earnings, Netflix gained as much as 4.1% after bouncing off support amid a descending triangle pattern. That said, the long-term uptrend from 2016 is broken as NFLX shares have fallen 37% over the past 52 weeks and are down 40% since the start of 2022, making it the worst performing FANG name of the past year.

{kind=link}

While Wall Street is still largely bullish, the number of holds has increased substantially in the past few months as the stock has been cut in half, and analysts today give the stock 31 buys, 17 holds and 3 sells; the average 12-month price target of $499.47 is 44% above the current price. But don’t hold your breath for a short squeeze: shares sold short equaled 0.5% of float, according to Markit data, down from 0.59% a month ago.

Which brings us to today, when after hitting an all time high around $700 in November, the stock has lost half of its value (and prompted Bill Ackman to build a substantial stake in the name), with investors on edge to find out not whether the company would beat its lousy guidance and recover some of its former torrid growth. Said otherwise, how many new subscribers did Netflix add in the fourth quarter.

Alternatively, failing to grow aggressively, perhaps – as Lightshed analyst Rich Greenfield asks – it is now time time for Netflix to announce an ad-supported tier. Recall that Disney+ recently said it was pursuing one, leaving Netflix as one of the streaming world’s glaring holdouts. CFO Spence Neumann has said it’s not in Netflix’s plans, but other industry executives say it’s inevitable.

Unfortunately for the bulls, this was not the quarter when NFLX was going to turn the business around because not only did the company report a huge miss to Q1 streaming subs but also guided to an even more catastrophic Q2 subscriber growth, when it sees a 2 million drop in subs vs expectations of a 2.4MM increase. The stock, needless to say, is imploding after hours and is down more than 20%!

Here is what NFLX reported for Q1:

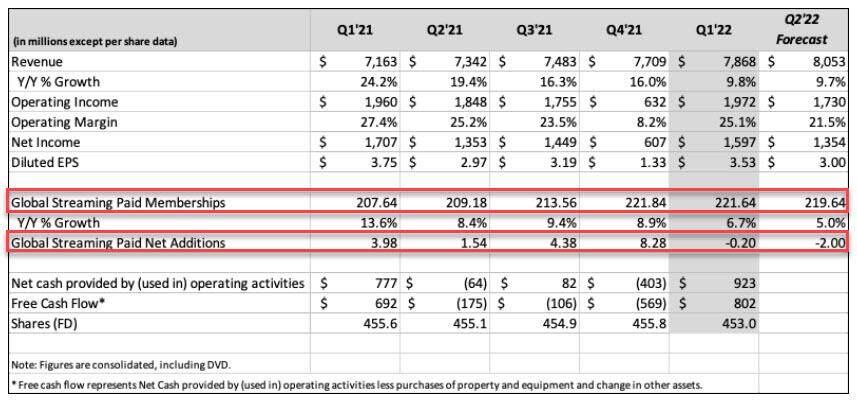

Revenue $7.87B, missing est. $7.95B

EPS $3.53, beating est. $2.91

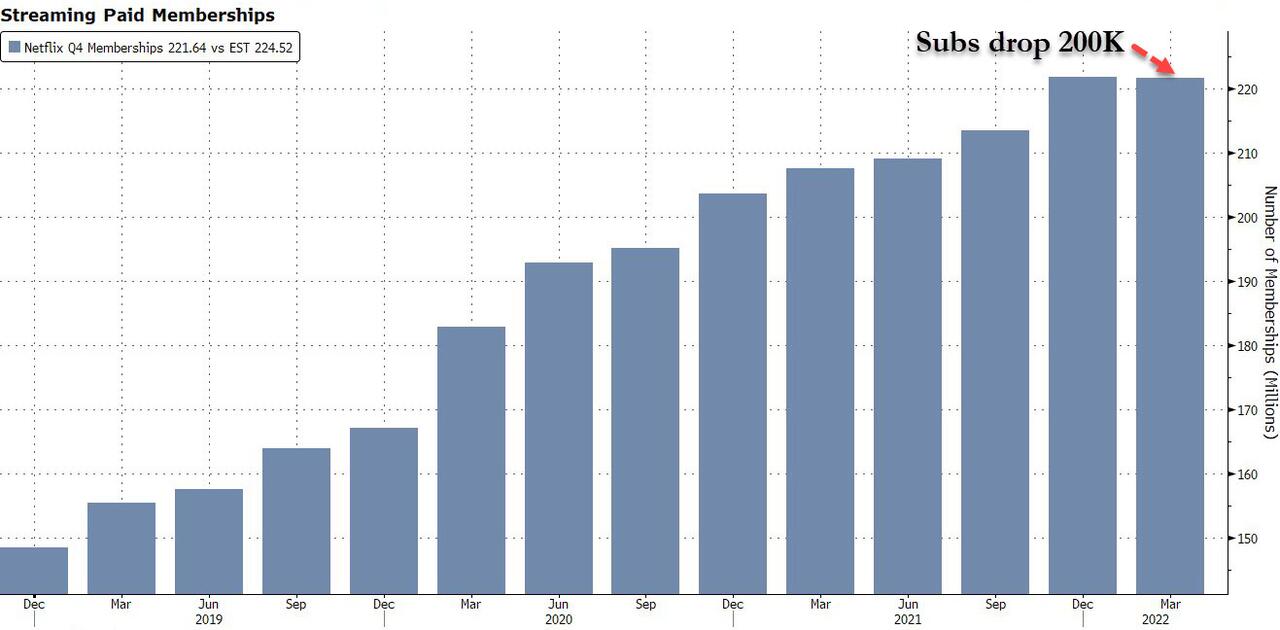

Streaming Paid Memberships 221.64M, missing the est. 224.5M

Netflix 1Q Streaming Paid Net Change -200,000, huge miss to the est. +2.5M

Yes, you read that right: NFLX reported a 200K subscriber LOSS in Q1, the first subscriber decline since 2011!

{kind=link}

This is a more detailed look at where the subscriber loss was:

Streaming paid net change -200,000 vs. +3.98 million y/y, estimate +2.5 million

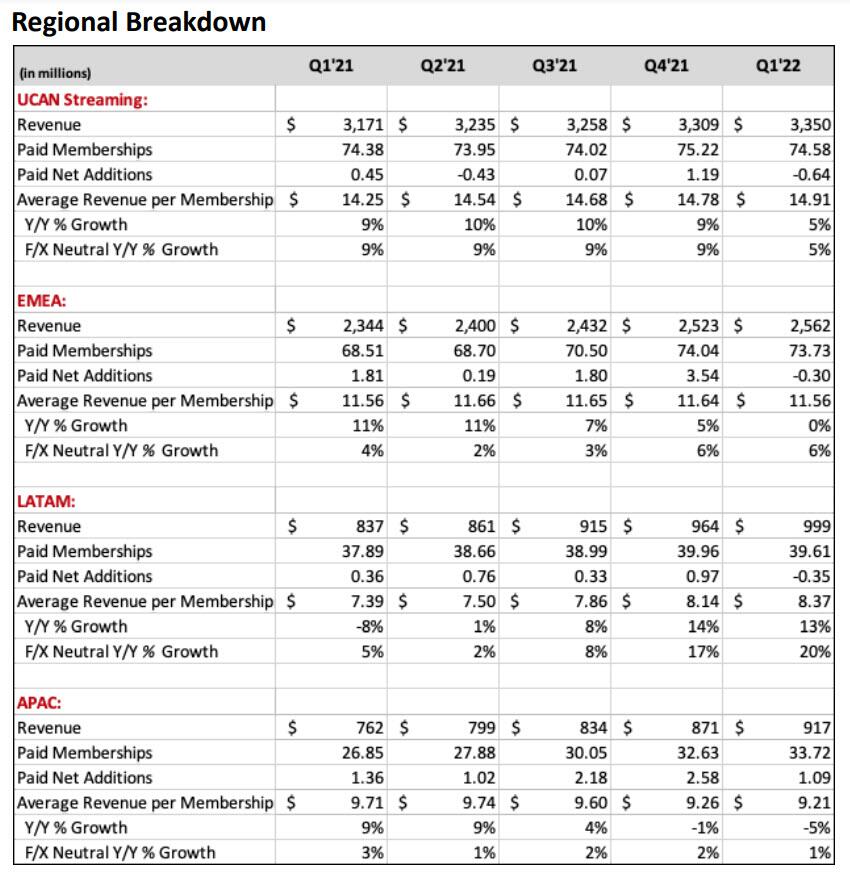

US/CANADA streaming paid net change -640,000 vs. +450,000 y/y, estimate +87,452

EMEA streaming paid net change -300,000 vs. +1.81 million y/y, estimate +950,354

LATAM streaming paid net change -350,000 vs. +360,000 y/y, estimate +334,429

APAC streaming paid net change +1.09 million, -20% y/y, estimate +1.2 million

With subscriber numbers sliding, and the torrid growth phase now over, NFLX is asking investors to focus on ARPU instead: “revenue and viewing will become more important indicators of our success than membership growth,” the company said in the shareholder letter… Just like when Apple stopped reporting iPhone sales figures.

While business predictably slowed in Central and Eastern Europe last month amid Russia’s invasion of Ukraine, the press release claims that activity is picking up in markets like Japan, India, and Taiwan. We’ll see. Remarkably, despite the recent price hike, NFLX’ average revenue per membership in the US rose just 5% to $14.91, with the growth rate slowing sharply from 9% just a quarter ago.

{kind=link}

This is how woke CEO, Reed Hasting, explained the huge miss – it was all the sharing households fault. At least it wasn’t Putin’s fault:

Our revenue growth has slowed considerably as our results and forecast below show. Streaming is winning over linear, as we predicted, and Netflix titles are very popular globally. However, our relatively high household penetration – when including the large number of households sharing accounts – combined with competition, is creating revenue growth headwinds. The big COVID boost to streaming obscured the picture until recently. While we work to reaccelerate our revenue growth – through improvements to our service and more effective monetization of multi-household sharing – we’ll be holding our operating margin at around 20%. Key to our success has been our ability to create amazing entertainment from all around the world, present it in highly personalized ways, and win more viewing than our competitors. These are Netflix’s core strengths and competitive advantages. Together with our strong profitability, we believe we have the foundation from which we can both significantly improve, and better monetize, our service longer term.

But if Q1 earnings were bad, the company’s guidance for Q2 was even worse where virtually everything missed and that was before the company said it now expected to lose 2 million subs!

Sees Q2 streaming paid net change -2.00 million, massively missing the estimate +2.4 million (Bloomberg Consensus)

Sees Q2 revenue $8.05 billion, missing the estimate $8.23 billion

Sees Q2 EPS $3.00, missing the estimate $3.02

Sees streaming paid memberships 219.64 million, missing the estimate 227.7 million

Sees operating margin 21.5%, missing the estimate 21.6%

{kind=link}

In other words, as BBG puts it, “the streaming service lost 200,000 customers in the first quarter, according to a statement Tuesday, the first time it has shed subscribers since 2011. Netflix also projects it will lose another 2 million customers in the current second quarter, setting up its worst year ever as a public company.”

Some more details on the dismal guidance:

Paid net additions were -0.2m compared against our guidance forecast of 2.5m and 4.0m in the same quarter a year ago. The suspension of our service in Russia and winding-down of all Russian paid memberships resulted in a -0.7m impact on paid net adds; excluding this impact, paid net additions totaled +0.5m. The main challenge for membership growth is continued soft acquisition across all regions. Retention was also slightly lower relative to our guidance forecast, although it remains at a very healthy level (we believe among the best in the industry). Recent price changes are largely tracking in-line with our expectations and remain significantly revenue positive.

In EMEA (-0.3M paid net adds, or +0.4m excluding the Russia impact), we saw a slowdown in our business in Central and Eastern Europe in March, coinciding with Russia’s invasion of Ukraine. Paid net additions in LATAM totaled -0.4M; similar to recent quarters, we believe a combination of forces including macroeconomic weakness and our price changes (F/X neutral ARM grew 20% year over year) were a drag on our membership growth. UCAN paid net adds of -0.6M was largely the result of our price change which is tracking in-line with our expectations and is significantly revenue positive. We’re making good progress in APAC where we are seeing nice growth in a variety of markets including Japan, India, Philippines, Thailand and Taiwan.

As a reminder, the quarterly guidance we provide is our actual internal forecast at the time we report. For Q2’22, we forecast paid net additions of -2.0m vs. +1.5m in the year ago quarter. Our forecast assumes our current trends persist (such as slow acquisition and the near term impact of price changes) plus typical seasonality (Q2 paid net adds are usually less than Q1 paid net adds). We project revenue to grow approximately 10% year over year in Q2, assuming roughly a mid-to-high single digit year over year increase in ARM on a F/X neutral basis. We still target a 19%-20% operating margin for the full year 2022, assuming no material swings in F/X rates from when we set this goal in January of 2022.

Here is the company’s justification for the first subscriber decline in a decade:

We’re not growing revenue as fast as we’d like. COVID clouded the picture by significantly increasing our growth in 2020, leading us to believe that most of our slowing growth in 2021 was due to the COVID pull forward. Now, we believe there are four main inter-related factors at work.

First, it’s increasingly clear that the pace of growth into our underlying addressable market (broadband homes) is partly dependent on factors we don’t directly control, like the uptake of connected TVs (since the majority of our viewing is on TVs), the adoption of on-demand entertainment, and data costs. We believe these factors will keep improving over time, so that all broadband households will be potential Netflix customers.

Second, in addition to our 222m paying households, we estimate that Netflix is being shared with over 100m additional households, including over 30m in the UCAN region. Account sharing as a percentage of our paying membership hasn’t changed much over the years, but, coupled with the first factor, means it’s harder to grow membership in many markets – an issue that was obscured by our COVID growth.

Third, competition for viewing with linear TV as well as YouTube, Amazon, and Hulu has been robust for the last 15 years. However, over the last three years, as traditional entertainment companies realized streaming is the future, many new streaming services have also launched. While our US television viewing share, for example, has been steady to up according to Nielsen, we want to grow that share faster. Higher view share is an indicator of higher satisfaction, which supports higher retention and revenue.

Fourth, macro factors, including sluggish economic growth, increasing inflation, geopolitical events such as Russia’s invasion of Ukraine, and some continued disruption from COVID are likely having an impact as well.

Translation: the kitchen sink list of excuses. Unfortunately for Reed, investors don’t care about excuses, they want results.

Looking ahead, how does Netflix hope to turn around the slowing business? Reed explains:

Our plan is to reaccelerate our viewing and revenue growth by continuing to improve all aspects of Netflix – in particular the quality of our programming and recommendations, which is what our members value most. On the content side, we’re doubling down on story development and creative excellence, which we see reflected in big Q1’22 TV hits like Bridgerton (627 million hours viewed for season 2 *, our 1 biggest English language series in our history) and Inventing Anna (512m hours viewed) – both from our extremely successful partnership with Shonda Rhimes – and films like Tinder Swindler (166m hours viewed, our biggest documentary film ever released) and The Adam Project (233m hours viewed), which come on the back of our Q4 hits Red Notice and Don’t Look Up. On the product side, we recently launched “double thumbs up” so members can better express what they truly love versus simply like – enabling us to continue to improve our personalized recommendations and overall experience.

This focus on continuous improvement has served us well over the past 25 years – from our big battle with Blockbuster nearly 20 years ago through the launch and growth of streaming, to the switch from licensed second run TV series and films to original programming, and our development from a domestic business with primarily English language content to a global entertainment service. It’s why we are now the largest subscription streaming service in the world on all key metrics: paid memberships, engagement, revenue and profit.

As discussed previously, Netflix hopes to crackdown on sharing, claiming that 100 million households are using another household’s account. In other words, NFLX hopes to tap into the untapped “thieves” market:

Another focus is how best to monetize sharing – the 100M+ households using another household’s account. This is a big opportunity as these households are already watching Netflix and enjoying our service. Sharing likely helped fuel our growth by getting more people using and enjoying Netflix. And we’ve always tried to make sharing within a member’s household easy, with features like profiles and multiple streams. While these have been very popular, they’ve created confusion about when and how Netflix can be shared with other households. So early last year we started testing different approaches to monetize sharing and, in March, introduced two new paid sharing features, where current members have the choice to pay for additional households, in three markets in Latin America. There’s a broad range of engagement when it comes to sharing households from high to occasional viewing. So while we won’t be able to monetize all of it right now, we believe it’s a large short- to mid-term opportunity. As we work to monetize sharing, growth in ARM, revenue and viewing will become more important indicators of our success than membership growth

For those curious, the company said that its biggest hits in the first quarter were “Bridgerton” (627 million hours viewed) and “Inventing Anna” (512 million hours viewed). Both are from Netflix’s deal with producer Shonda Rhimes. Other popular films included Tinder Swindler (166m hours viewed, the biggest documentary film ever released on NFLX) and The Adam Project (233m hours viewed).

Looking at NFLX free cash flow, the company reported that net cash generated by operating activities in Q1 was $923 million vs. $777 million in the prior year period. Free cash flow amounted to $802 million vs. $692 million, and NFLX continues to “expect to be free cash flow positive for the full year 2022 and beyond.”

It wouldn’t be a Netflix report without inserting the usual “get woke, go broke” line in there somewhere.

{kind=link}

After all that, investors were not impressed the stock has gotten absolutely monkeyhammered after hours, plunging 20% on these catastrophic earnings which sent NFLX stock below $280 to the lowest level since October 2019!

{kind=link}

NFLX results were so bad, all the company’s peers are tumbling after hours, and among streaming peers: Roku -6.1%, Walt Disney -3.5%, fuboTV -3.8%, Paramount Global -4.5%, Warner Bros Discovery -2.4%. Among other major technology and internet stocks: Amazon.com -0.9%, Microsoft -0.5%, Meta Platforms -1.2%. Why? Because as Bloomberg notes, Netflix’s forecast for a loss of two million subscribers in the current quarter is likely to prompt analysts to rethink their forecasts for the entire industry, as “the industry leader is suggesting a plateau of subscribers may be at hand, particularly in the U.S. market, where Netflix reported its largest subscriber drop in the first quarter.”

What’s next? Nothing pretty…

Before it’s all over, NFLX will be shipping out DVDs again

— zerohedge (@zerohedge) April 19, 2022

Tyler Durden

Tue, 04/19/2022 – 18:25

Please follow and like us: