Trump Did It: Executives & Administrators Are Increasingly Using TDI To Fight DEI Authored by Jonathan Turley, “Trump made me...

Read More

Gordon Johnson: Tesla Just Went “Ex-Growth”, Last Quarter’s EPS Was Helped By $1/Share In Non-Core Items

Perpetual Tesla critic and proprietor of GLJ Research, Gordon Johnson, was out late last week with a new note to clients explaining why Tesla’s numbers, to him, look similar to the growth fall off that Netflix just experienced.

Johnson claims in his latest note that Tesla’s $2.87 in GAAP EPS that the company just reported was helped along by $1/share in non-core items.

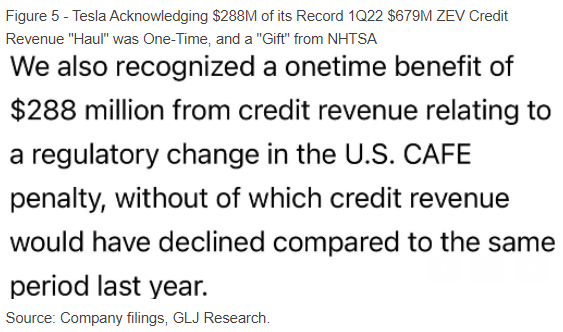

“In short, when adjusting for (a) $288M in one-time regulatory cafe credits “gifted” to TSLA by NHTSA four days prior to quarter end, (b) $377M in “magical” cost reductions (TSLA’s OPEX fell from $2.234B to $1.857B, despite 40yr high inflation, two new plants ramping, and flat unit production – we believe a lot of this had to do with capitalized TX/Berlin costs, as well as lower SBC for E. Musk), and (c) $497M in incremental non-current other assets (which, based on TSLA’s 10-K filing, consists of pure margin benefit long-term government rebates), TSLA’s $2.87/shr in GAAP EPS was helped by ~$1.00/shr in non-core items,” Johnson’s latest note says.

{kind=link}

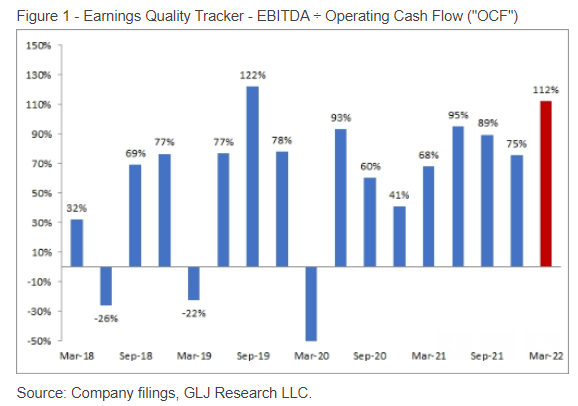

He continues, explaining that the quality of Tesla’s earnings has deteriorated: “This can be further seen in the significant erosion in the quality of TSLA’s earnings this quarter, using (EBITDA ÷ Operating Cash Flow) as a ‘measuring stick’ – this metric advanced to the highest/worst level in 1Q22 since 3Q19.”

{kind=link}

Johnson says that Tesla’s valuation telegraphs “big problems” ahead:

Furthermore, when considering TSLA is trading at ~100x annualized 1Q22 earnings, yet didn’t grow units in 1Q22 (and will see unit sales fall in 2Q22), and operates in an auto industry that trades, on avg., at 6.1x forward earnings, we see (big) problems ahead.

He also commented about Shanghai still being shut down, stating that he thinks Elon Musk “likely lied” when he claimed on the conference call that “the most likely vehicle production in Q2 will be similar to Q1, maybe slightly lower, but it’s also possible we may pull a rabbit out of the hat and be slightly higher”.

Johnson wrote to clients: “In short, we believe E. Musk saw the move in Netflix’s stock ex-growth in [last week’s] trading session, and wanted to paint a picture that, no matter what, TSLA will not go ex-growth, on a unit sales basis, in 2Q22 (we believe his forecast here will prove [very] wrong).”

Tyler Durden

Tue, 04/26/2022 – 05:45

Please follow and like us: