Trump Did It: Executives & Administrators Are Increasingly Using TDI To Fight DEI Authored by Jonathan Turley, “Trump made me...

Read More

A Plethora Of New Macro Trends

We are currently experiencing profound changes in the global economy that are likely to unleash a plethora of early-stage secular trends in a new inflationary regime. These are long-overdue structural shifts powered by decades of easy money policies and record levels of debt-to-GDP among developed economies:

Governments and central banks to seek high-quality international reserves in attempt to restore the credibility of fiat currencies; gold will play a major role as a monetary asset

Monetary metals and other tangible assets to regain relevance in crowded 60/40 portfolios as inflationary hedges

Central banks ultimately forced to cap long-term yields creating a major tailwind for inflationary assets

The beginning of a commodities cycle after chronic under-investment in natural resource industries

A new “Exploration Age” for commodities as major producers address their supply cliff

Deglobalization trends prompt a long-overdue manufacturing re-build in developed economies including a boost to non-residential construction

Rising geopolitical tensions spur increase in defense spending from historic low levels compared to GDP

The continuation of one of the most extensive fiscal agendas in history, driven by the Green Revolution, social equality programs, infrastructure revamp, and defense spending

Ongoing flood of sovereign debt issuances and persistent inflationary pressure to cause long-term interest rates to rise globally

Overall corporate margins to be squeezed by the rise in cost of capital, commodity prices, and labor cost as the Fed tightens monetary conditions

The resurgence of fundamental analysis and value investing principles as profitability becomes a priority

A re-pricing of long duration growth stocks from record valuations as cost of capital increases

A major shift in market leadership from technology to natural resources related businesses

Geopolitically neutral and commodity-driven economies to gain relevance on the global stage, i.e. Brazil

Upcoming challenges to historically indebted net importers of commodities, i.e. China

Unparalleled to any other time in history, the current macro imbalances have drastically distorted the market perception of value and risk. This scenario is setting the stage for significant changes in portfolio allocations from crowded and overvalued assets to unloved and historically cheap alternatives. For macro investors, we think this is one of the most opportunistic times ever.

Let’s dive in on each of these themes to share our detailed views about the global economy.

Natural Resource Under Investments

If there was ever a time to own tangible assets and businesses that benefit from the appreciation of these underlying assets, that time would be now. Ultimately, the sustainability of commodity bull markets is predicated on the spending trends for natural resource industries. By and large, these are long-term cycles that take time to reverse. Years of misallocation of capital, equity dilution, corporate mismanagement and money-losing operations have now turned into excessive conservatism. When adjusted for GDP levels, the aggregate capex for commodity producers remains lower than it was in 2003, almost 20 years ago.

{kind=link}

Cash-Flow Machines

Natural resource industries are now generating more free-cash-flow than any other time in history. To be exact, they reported three times more annual free-cash-flow than their historical peak. While these companies have turned into incredibly profitable businesses, they have yet to become new darlings for investors.

{kind=link}

Early Signs

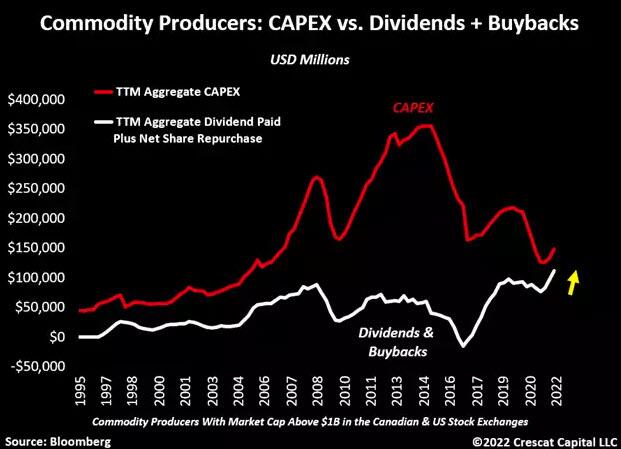

Commodity producers remain so financially restrained to invest in their businesses that they are almost giving more capital back to shareholders than what they spend on CAPEX. In the last year, nearly 30% of the cash flow from operations generated by these companies was spent on dividends and share buybacks. The chart below reflects how natural resource industries are more focused on attracting investors by these shareholder friendly actions than through trying to grow their businesses. This is a classic sign of a commodities cycle in its early innings.

{kind=link}

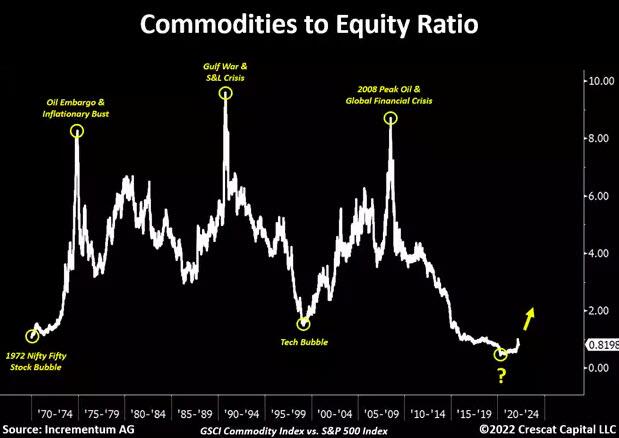

How can anyone claim commodities are overextended when prices relative to overall equity markets remain near 50-year lows? Every time we reach such suppressed levels in this ratio it marked the beginning of commodities cycles. The chart below is an incredible illustration of the opportunity still ahead of us. The credit goes to our good friends at Incrementum AG for always providing outstanding research.

{kind=link}

In our Global Macro, Long Short and Large Cap strategies, we hold a large and diversified position in raw materials businesses on all fronts, including metals, energy, agriculture, and forest products. On a side note, we do think that gold and silver miners, more than any other natural resource industry, are overdue for a major catch-up with their peers.

Here is one interesting fact to consider: precious metals mining companies are not only the most profitable they have ever been in history, but they also have the strongest operating margins among all other commodity producers. That is despite the recent increase in energy prices and surge in labor costs.

{kind=link}

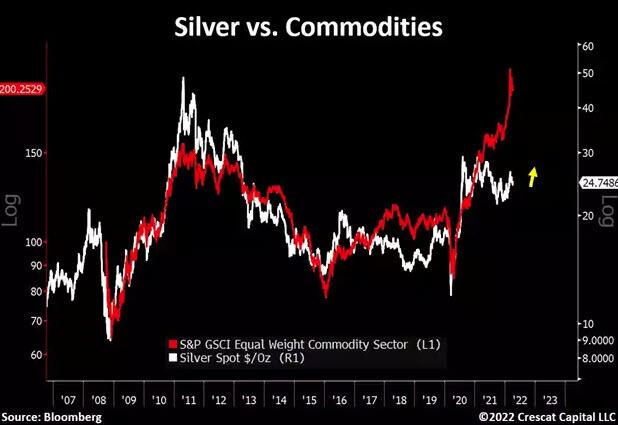

Silver remains one of the most mispriced opportunities in financial markets today. While the overall commodities market has drastically risen, this high-beta version of gold remains at historically cheap levels. If silver were to just catch up to the move in other tangible assets, it would imply a doubling from current levels.

{kind=link}

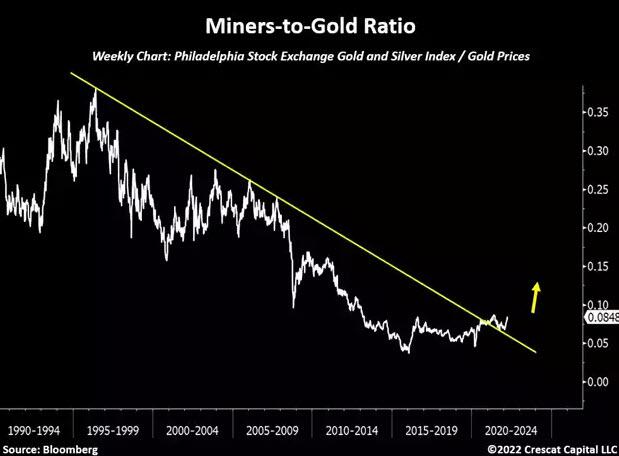

Precious metals companies have been performing incredibly well recently despite the significant rise in US Treasury yields. Remarkably, the industry has underperformed gold prices for over 26 years. With rising profitability, balance sheet improvements, extreme capital spending conservatism by corporate management, there is so much value still to be unlocked in this industry.

{kind=link}

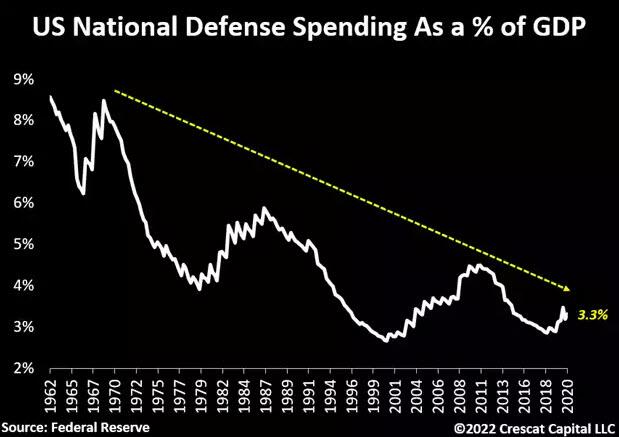

Defense Spending Resurgence

The Russian invasion of Ukraine has marked a tectonic shift in the geopolitical landscape with innumerable long-lasting ramifications. The trade deglobalization trend that had already begun with respect to disengagement with China is only more likely to continue now and brings with it long-lasting inflationary implications.

We further believe that US defense spending is now set to increase drastically from current historic low levels of GDP. If the US were to move back to Cold War spending levels, we could see a doubling from here to about 6.6% of GDP which would unleash $1.5 trillion of new government spending. But even half or a quarter of that amount would be an extraordinary boost to the defense industry that has a total market capitalization of just $500 billion and a mere $240 billion in annual revenues today. Other NATO countries are also likely to drastically increase their defense budgets. We have already started buying US defense companies that are supported by our equity model in our Global Macro, Long Short and Large Cap strategies.

However, with military spending ripe to go significantly higher from here, it will only further fuel the inflationary problem due to increased deficit spending. The US is already facing one of its worst fiscal imbalances ever while running one of its lowest defense budgets in history.

{kind=link}

A Manufacturing Revamp Ahead of Us

After many decades of benefiting from a highly globalized world economy, US corporations will likely be forced to re-establish their manufacturing plans domestically to avoid international reliance on labor and supply resources. These shifts may drive the long-overdue revamp of American infrastructure. A potential uptrend in non-residential construction from historic lows could substantially boost the demand for commodities.

{kind=link}

“Gold is Money, Everything Else is Credit”

Once again, gold is playing a major role serving as a monetary asset and tangible anchor for fiat currencies. As insane as it sounds, the most credible central bank balance sheets today are the ones that have built that reputation by owning debt of other massively levered economies. As shown in the chart below, this is already in the process of changing.

After many years of strong positive correlation with fixed income securities, gold is now rising despite the historic rout in global bonds. In our view, global bonds yielding negative in nominal terms are about to become obsolete. Their overall outstanding value just went $18 trillion to less than $3 trillion. Outflows from fixed income markets are likely to become inflows for tangible assets like gold. With rising inflation, particularly among developed economies, central banks and governments are being forced to improve the quality of their international reserves as an attempt to restore the credibility of their monetary systems.

{kind=link}

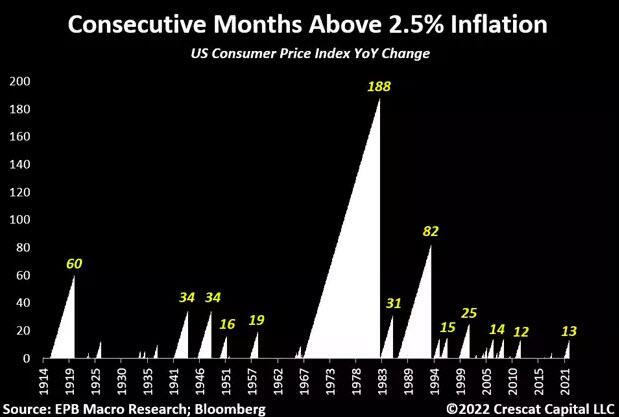

Five Pillars of Inflation

We are currently facing five early-stage structural changes in the macro environment that are likely to fuel a long-term inflationary problem:

The “demand-pull” from rising wages and salaries and a tight labor market

“Cost-push” supply shortages caused by a chronic period of under-investment in natural resource industries

Reckless fiscal spending

Rising deglobalization trends

The need to deleverage debt-to-GDP though rising inflation

As shown on the chart below, we have only seen 13 consecutive months where CPI stayed above 2.5%. This measurement puts into perspective how much longer CPI stayed above such levels during other inflationary regimes that also experienced similar macro forces serving as tailwinds for consumer prices.

{kind=link}

Inflation is concerning but the real issue is how policy makers are dealing with the situation. Amid the highest CPI prints in 40 years, today we have one of the most aggressive fiscal policies in history for how strong the labor market is. Hard to believe inflation will cool off from here. The Fed’s interest rate hikes can cool demand but work against the need to help finance an increased supply of critical resources.

{kind=link}

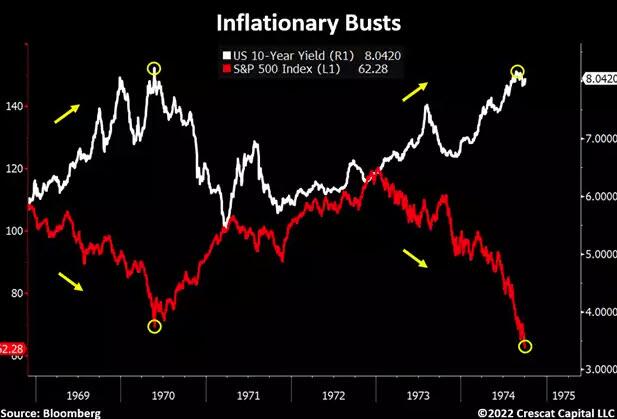

Inflationary Crises

Bonds have served as incredible hedges during the last several downturns in equity markets. The rising inflation environment that led up to the tech and housing busts proved to be a cyclical force as the economy entered a significant downturn and nominal yields collapsed as a result. Inflation also decelerated drastically during the Covid crash in March 2020 and long-term rates declined in tandem. We fear investors are “fighting the last war” in expecting the same correlation to play out in the next major equity downturn. The structural changes in inflation today are causing this relationship to change drastically. Market participants are conditioned to think of sovereign bonds as safe havens, but that was not a reality during other inflationary regimes.

In 1968-69 and 1973-74, as equity markets collapsed and the economy entered a recession, long-term nominal yields increased instead. Such market developments are consequences of an economy facing long-term inflationary pressure rather than cyclical forces. We think Treasury yields and equity market correlations will look similar in the next recession.

{kind=link}

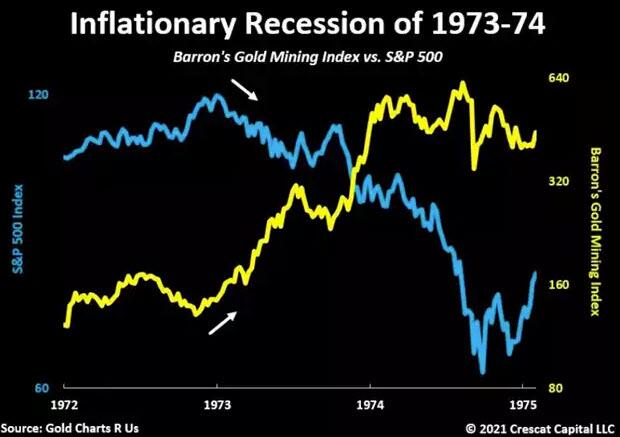

Gold and Miners Prevail During Inflationary Crises

Contrary to today’s conventional wisdom, note how gold miners increased 5-fold while the stock market declined 50% during the 1973-74 inflationary recession. We think a similar development will follow in the next economic downturn.

{kind=link}

But does today’s macro setup really resemble the 1970s?

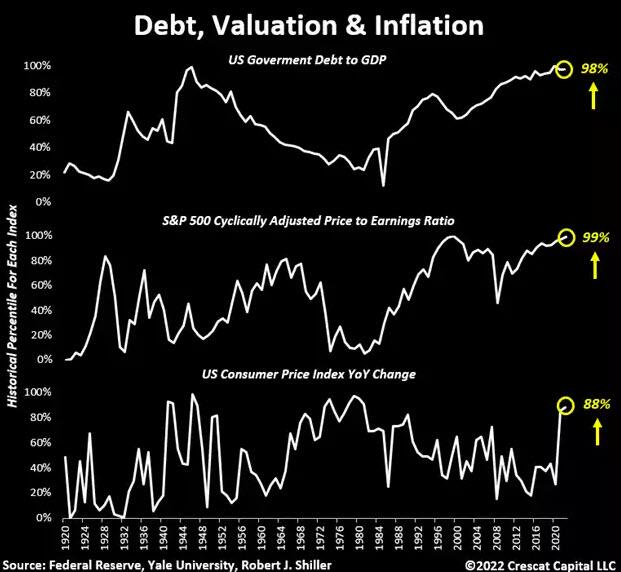

As tempting as it can be, the use of any one point in history as a guide may offer an incomplete assessment of what is likely ahead of us. For the first time in 120 years, the US economy is facing a trifecta of economic extremes. We need to combine the debt problem of the 1940s, the structural commodity shortages of the 1970s, and the speculative equity valuation environment of the late 1920s and 1990s in order to get a more complete picture of the macro setup that we have today. These imbalances create true political constraints to governments and central banks. It is hard for us to believe how inflation will not continue to be one of the major forces infiltrating the economy over the next several years to reconcile these imbalances.

{kind=link}

Peak of the Business Cycle

We are seeing a list of recession indicators flashing warning signals today. Beware of times when the spread of consumer confidence “present situation” vs. “expectation” is at cyclical highs. Last time this spread was as extreme as today was right before the tech bust and the 1973-4 recession.

{kind=link}

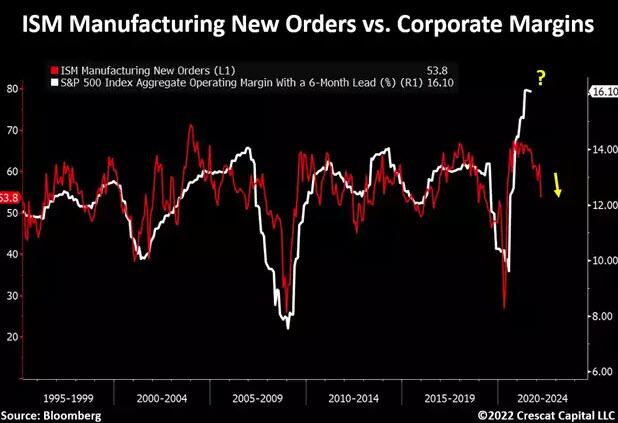

Corporate Margins at Risk

The rise in material prices, wages, and now cost of capital is likely to truly impact corporate margins. To recall, earnings always reach a cyclical top at the peak of the business cycle. We think this time is no different. Similarly, labor markets tend to be very reliant contrarian indicators. The U-3 unemployment rate and initial jobless claims are both at one of the lowest levels in history.

{kind=link}

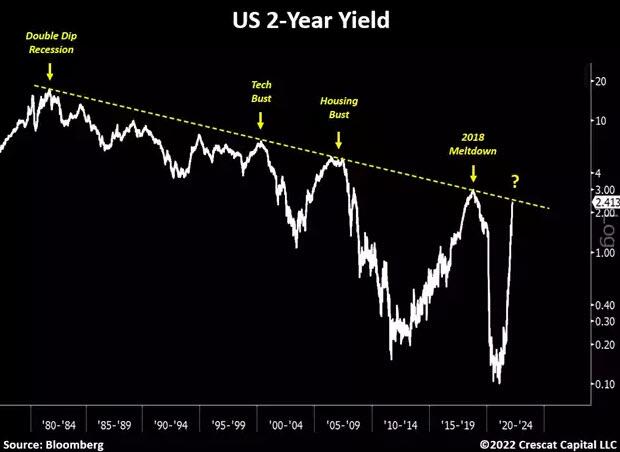

Eerie Resemblance

The US 2-year yield just re-tested its multi-decade resistance. This move happened four other times in the last 40 years, and all of them were followed by significant economic downturns.

We are likely at the peak of the business cycle. While we think the 2-year yield could easily break out above this trend, finally, it won’t change our view about a major deceleration of growth after inflation ahead. Given the current political constraints, it is a 1973-74 setup on steroids.

{kind=link}

Tech Bubble 2.0

This could be just a coincidence, but the S&P 500 technology sector is almost as overvalued relative to the overall market as it was at the peak of the tech bubble. Note that the ratio perfectly re-tested the same level we saw in March 2000 right before technology companies suffered from a severe bear market in the next two years. We think this sector is unlikely to be the next sector to lead equity markets and these companies are at major risk of being re-rated at significantly lower prices relative to their fundamentals.

{kind=link}

Insanely Speculative

Easy-money policies and excess liquidity have created one of the worst asset valuation distortions in history. Almost every fundamental multiple that we track is currently at historically expensive levels. To put into perspective, US market cap to GDP needs to fall another 15% just to reach peak Tech Bubble levels.

{kind=link}

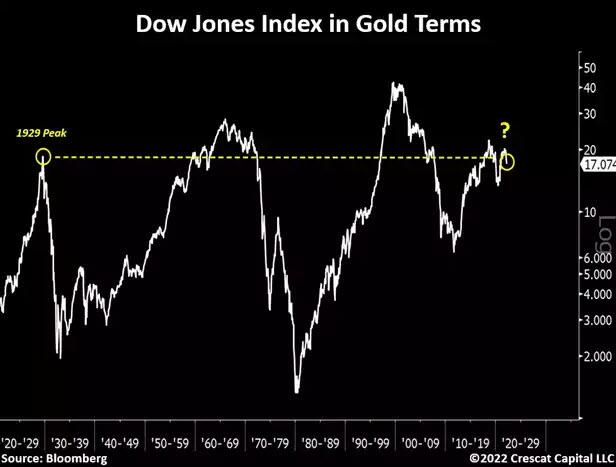

US Stocks vs. Gold

Not to be overlooked, US stocks in gold terms are just as expensive as they were at the 1929 peak prior to the Great Depression.

{kind=link}

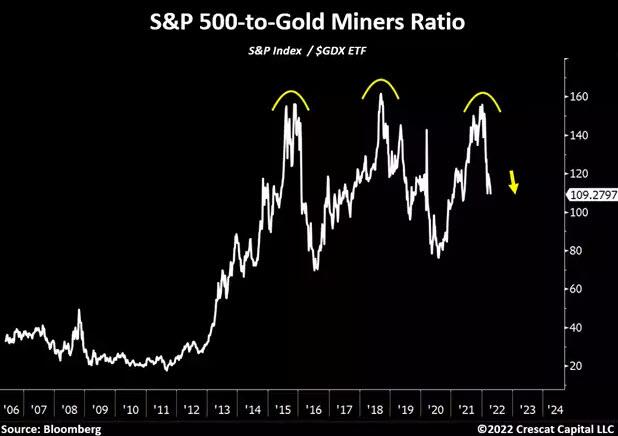

Sell Overall Stocks & Buy Gold Miners

We believe S&P 500-to-gold miners ratio is headed lower from here. The macro and fundamental case for owning precious metals companies vs. overall equities has never been more attractive.

{kind=link}

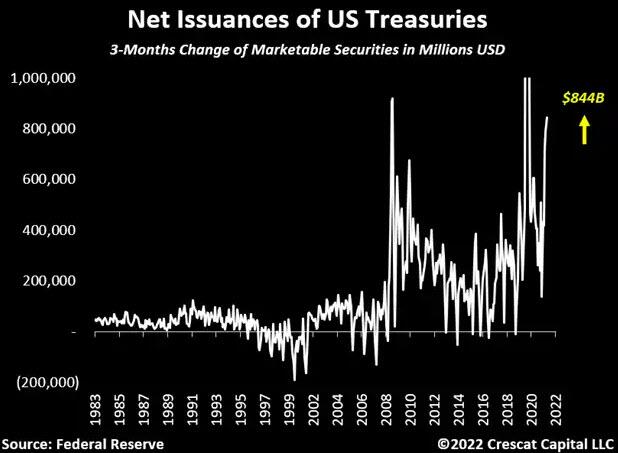

Flood of Treasury Issuances

While most market participants often focus on the demand factors for US Treasuries, we think the supply side of the argument remains the most relevant part of our bearish thesis. We are experiencing a flood of Treasury issuances as of late. Just in the last three months the government issued over $840 billion of these instruments amid the worst inflationary problem in 40 years. Meanwhile, the Fed just went from being the largest buyer of Treasuries to now wanting to become a seller.

{kind=link}

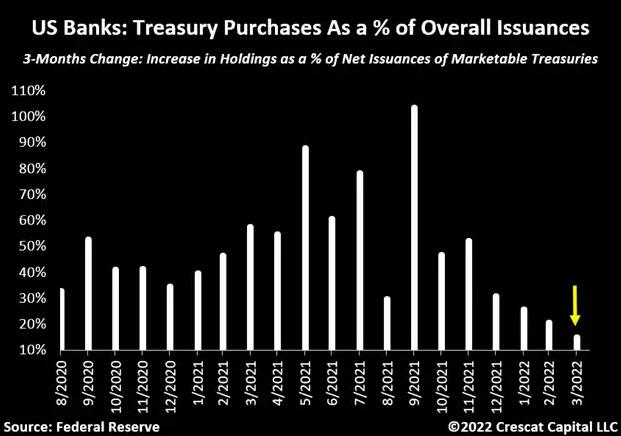

In addition to the Fed’s policy reversal, US banks, which supposedly should be making up for the lower demand from other parties, only purchased about 20% of overall US debt issuances.

{kind=link}

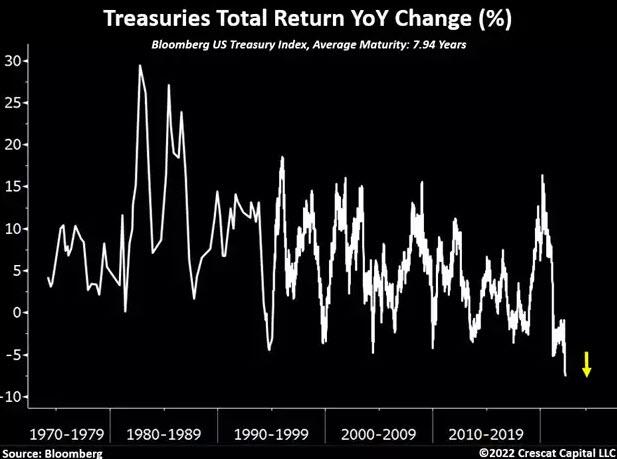

Where We Think Nominal Yields Are Headed

After the largest annual decline in US Treasuries in 50 years, we think these instruments are looking significantly oversold in the short term. Therefore, we expect a relief rally before another bigger selloff. In a similar fashion to what is unfolding in Japan, we think the Fed will be forced to cap long-term yields.

How high are they likely to go? We think it is unnecessary to answer this question now. As usual, policy makers should be very vocal when long-term yields get too high and become an issue.

We also believe that any potential increase in the balance sheet assets to suppress nominal rates would create a massive tailwind for a massive surge in inflation-hedge assets. This policy reversal might be what causes gold to move violently higher in price.

{kind=link}

Energy Shortage

Given the macro and fundamental backdrop, we continue to be buyers of oil and gas businesses. These energy companies are currently generating more free-cash-flow than any other time in history. Meanwhile, political efforts towards ESG policies are still preventing them from performing at full capacity which remains very bullish for commodity prices. In fact, oil production still is almost 10% lower than it was at its prior peak in February 2020.

{kind=link}

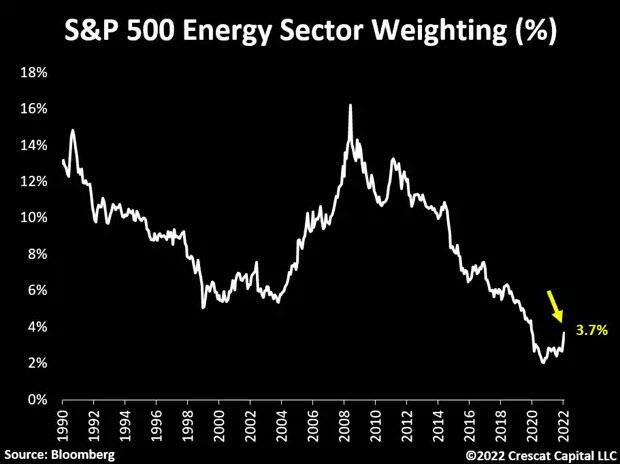

Essential to Function the Economy but Priced as Irrelevant

A reminder that the energy sector makes up less than 4% of the S&P 500 weight today, which remains to be one of the lowest levels ever.

{kind=link}

Energy Disconnect

The performance by sector in the US equity market since the pandemic lows has been astonishing. The disconnect in energy stocks simply reflects the macro regime we just entered.

{kind=link}

Brazil: Geopolitically Neutral & Commodity-Driven Economy

Brazil is one of the few economies in the world that could do exceptionally well in today’s macro environment. It is a commodity-driven economy with a long history of dealing with inflationary problems and political shifts. From a value perspective, Brazilian equities are just as undervalued as they were at the early stages of a multi-year bull market in early 2000s. The upcoming elections add a degree of uncertainty and fear, but at such attractive prices we think the risks are mostly priced in. Historically, the Brazilian economy has an incredibly strong correlation to commodity markets. We view this opportunity as a high-beta version of our long positions in natural resources. Different than the Fed, the Brazilian central bank has gone long ways to proactively tighten financial conditions as inflation gained momentum. Short-term interest rates, also known as Selic rates, went from 2% to 11.75% in the last 13 months. Inflation remains elevated but slightly below interest rates. Brazil is one of the few economies in the world running a positive real interest policy.

See below the price-to-sales differential between Brazilian and US equities.

{kind=link}

China Yuan Devaluation

The relative performance of Chinese vs. US stocks has been dismal. Meanwhile, the yuan remains unsustainably strong, though is finally starting to slip. The economy with the largest credit imbalance in the world has been grinding to a halt. The People’s Bank of China has no choice but to loosen credit conditions to counter its real estate and stock market implosion. At the same time, the Federal Reserve has no choice but to raise interest rates to fight inflation. The renminbi is at risk of a major devaluation.

{kind=link}

The PBOC is easing while the Fed is tightening, and that is only likely to continue with many lead indicators signaling much further yuan devaluation ahead. That is the crux of it, and it’s a big deal. Crescat’s asymmetric laddered long USD vs. CNH call options in the Global Macro fund have been performing extremely well in April MTD. We think there is much more to play out.

{kind=link}

A Final Note on Gold

We have been in a de facto Bretton Woods system for the last several decades with many parallels today to the 1968 to 1971 period. Like then, there is a good chance we are about to move away from a system of Western central bank cooperation. The need to deleverage debt-to-GDP globally with fiat currency devaluation is being met with a serious structural global commodity supply shortage.

Western central bank coordination has kept gold suppressed versus dollars, euros, yen, etc. It has also created historic debt-to-GDP levels in these countries creating tremendous pressure on the system. Here is the best macro academic paper on the Collapse of the London Gold Pool and end of Bretton Woods: https://economics.ucdavis.edu/events/papers/copy2_of_417Bordo.pdf. It is a must-read because it discusses the bigger issues surrounding “central bank cooperation”.

We need to remember that it was inflation, not deflation as posited by the Triffin dilemma, that led to the breakdown of the Bretton Woods system. We face the same problem today. Due to an unsustainable set of macro extremes, inflation has become unhinged and will likely only continue to spiral. Many will be slow to abandon their belief that too much debt in the world means we will necessarily face deflation. At this juncture, we think people will be better served by coming to the realization that inflation is the ultimate path of least resistance to deleveraging debt to GDP.

With France having repatriated its gold from the UK recently, it echoes De Gaulle breaking from the London Gold Pool in 1968. Even with the writing on the wall at that time, it was not until 1971 that the dam broke. Forward thinking investors today likely still have time to get ahead of the curve, but who knows exactly how much time?

Soon enough, individual investors, institutions, and central banks themselves will be breaking from the Western sovereign debt and fiat cabal and grabbing for the gold. At Crescat, we have always referred to the inherent problem with central bank cooperation as a “prisoner’s dilemma”, a game theory problem that ensures the ultimate breakdown of the entire system. It has taken a long time to get here, but we believe we are finally on the precipice.

Contrary to much gold conspiracy thought, it does not mean that we are facing the demise of the Western banking system nor the rise of authoritarian economies and their fiat currencies. It doesn’t necessarily mean the rise of non-government backed intangible currencies either. Governments will maintain legal authority and power over currency systems. Individuals and businesses will use those currencies. The strongest fiat currencies are likely to continue to be those in advanced economies where the principles of liberty, justice, democracy, entrepreneurship, and free markets reign.

The macro setup today portends a deleveraging of the global economy through inflation, including a probable step-function devaluation of all fiat currency systems relative to gold, a persistent phenomenon throughout world history.

Tyler Durden

Tue, 05/03/2022 – 11:29

Please follow and like us: