Trump Did It: Executives & Administrators Are Increasingly Using TDI To Fight DEI Authored by Jonathan Turley, “Trump made me...

Read More

Here’s What The Fed Will Say Today And How To Decide If It’s Hawkish Or Dovish

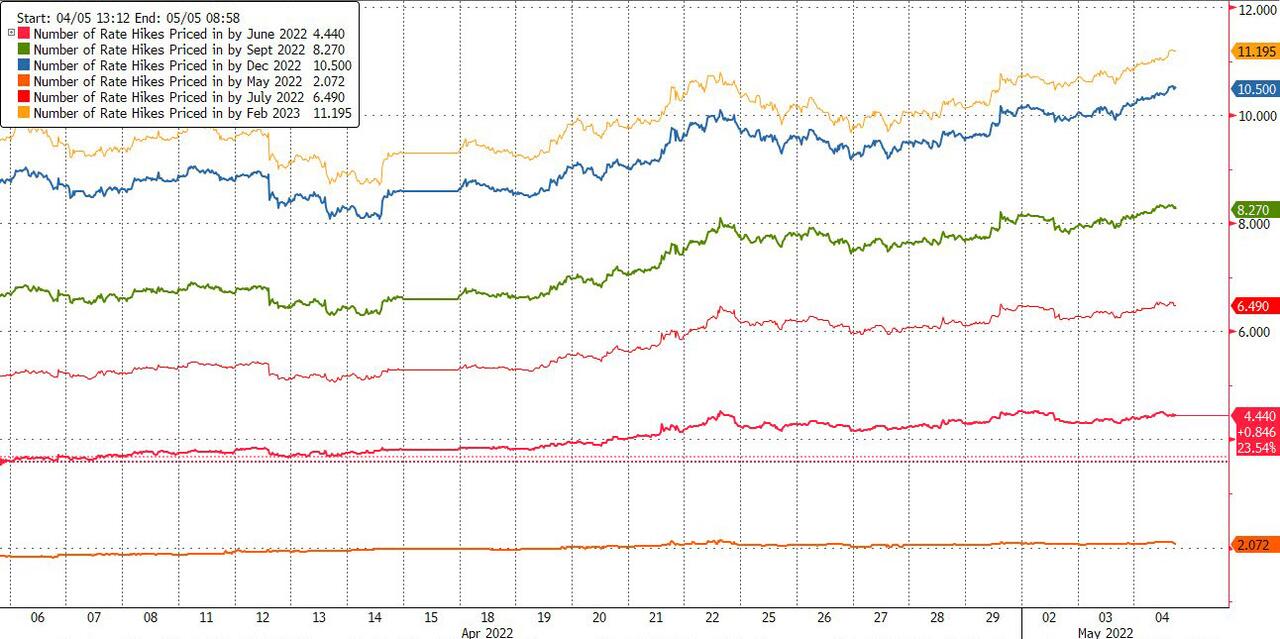

We already did not one but two lengthy FOMC preview (the first one is what the Fed will do, the second one is why what the Fed will do may be even more hawkish than most expect), so we won’t waste readers time with even more analysis of what the market expects things to get – below we show the latest rate hike odds chart indicating 100%+ odds of a 50bps raise (2 rate hikes) today, as well as the next three consecutive Fed meetings (in May, June, July and September) including almost 50% odds of a 75 bps rate hike in June – which eventually rise to more than ten 25bps rate hikes through December 2022…

{kind=link}

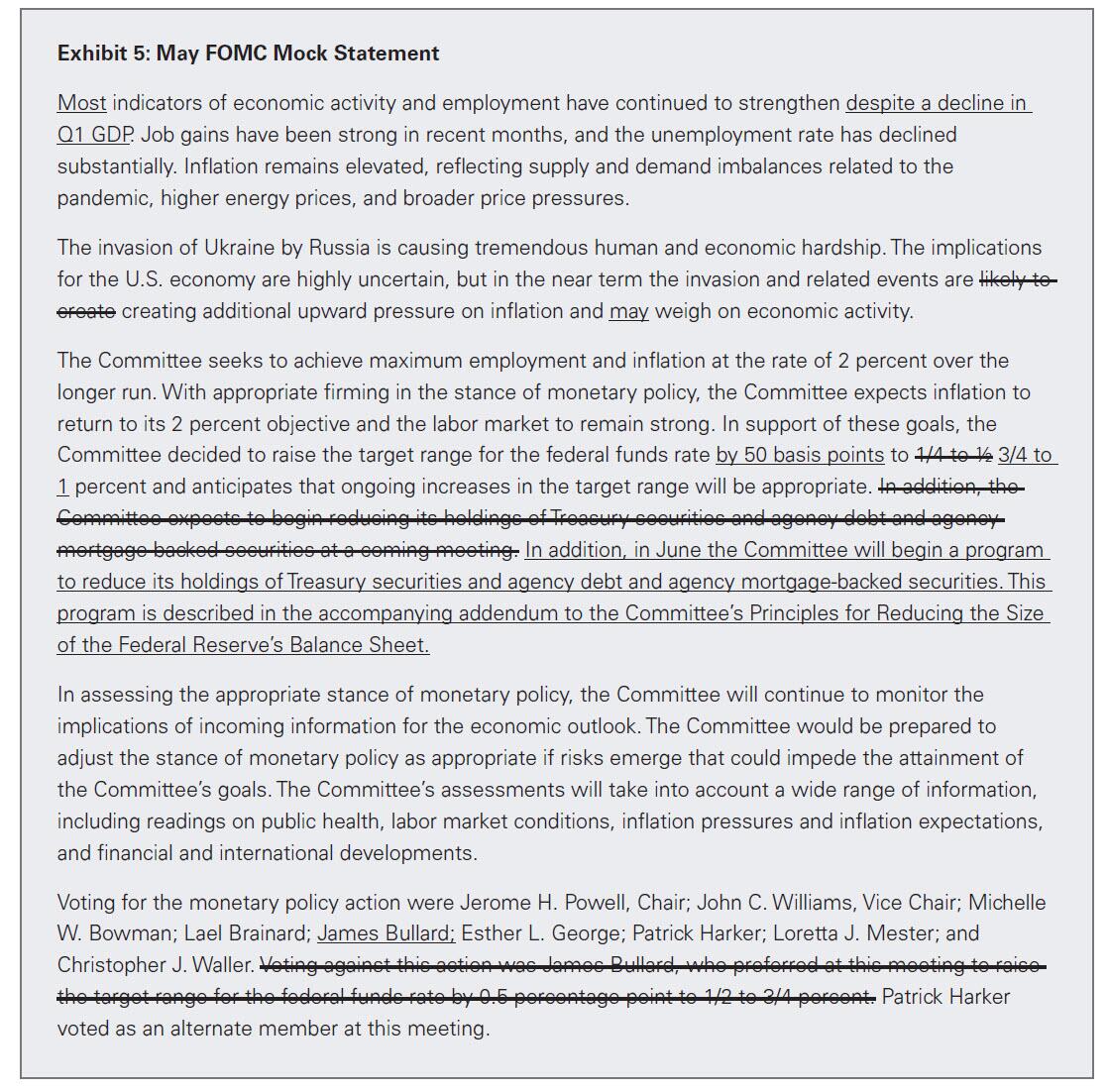

… and instead we will simply publish Goldman’s proposed redline statement of what the Fed will do today (there is much more in the full Goldman preview note available to professional subscribers).

{kind=link}

For those who missed our preview, today the Fed will announce a 50bps hike (JPM sees a 1 in 5 chance of a 75bps hike) and the start of QT. The parameters were largely announced in the March minutes so the main event will be Powell’s stance in the presser. For this I look to the quote below at the IMF panel for his most current thinking: they are not waiting to see the peak in inflation to move expeditiously to neutral. This notion has been repeated by almost every Fed speaker to indicate the path between now and year-end

Of course, much of today’s Fed communication will come from Powell during the FOMC presser where a hawkish surprise may be more likely to emerge, so pay attention there whether the Fed will hike 50 or 75bps in coming months, and also for some additional clarity on the Fed’s balance sheet reduction plans. As a reminder, the Fed will announced QT which will begin in June and take 3 months to ramp up to the $95bn/month cap, comprised of $60bn for Treasuries and $35bn for MBS. As discussed last night, the most relevant part of the meeting will be the language for forward guidance and whether that gives any hints as to a 75bps hike or changes to QT cadence.

In their preview of the FOMC, JPM’s rates traders have a neutral stance heading into the Fed as “the Rates market is pricing in 200bps of hikes over the next 4 Fed meetings and valuations are looking cheap.” With markets pricing in neutral rates policy, investors are increasingly looking at the short-end of the yield curve to find value. The erosion of risk premia in the yield curve likely means that the most dramatic moves in bonds this year are now behind us. For Equity investors, a reduction in bond vol could mean seeing the VIX reprice lower, too.

Finally, speaking of JPM’s flow desk, here is their summary of potential outcomes:

POTENTIAL OUTCOMES

HAWKISH

Change in statement to highlight return to neutral: “continue to expeditiously remove accommodation.”

Usefulness of 75bps noted vis-à-vis the 1994 experience (see Bullard below)

Powell quotes a neutral rate or range of neutral rate that is at or higher than the 2.375% in the presser

QT implementation note to include language on sales as in the balance sheet normalization plans (“In the longer run, the Committee intends to hold primarily Treasury securities in the SOMA”) or the March FOMC minutes (“after balance sheet runoff was well under way, it will be appropriate to consider sales of agency MBS to enable suitable progress toward a longer-run SOMA portfolio composed primarily of Federal Open Market Committee Treasury securities.”)

QT implementation note or press conference supports the idea that any reinvestments above the cap could move to front-end USTs only (a change to the current proportional add-on process)

QT May start and caps less than 3Ms

Anything that indicates QT could be used to more specifically target inflation

NEUTRAL

No change to statement: “anticipates that ongoing increases in the target range will be appropriate.”

Use of expeditiously in the presser to describe pace to neutral

Borrows language from Williams and Brainard to be vague about the actual level of neutral

QT June start, 60bn UST/35bn MBS phase in period of 3months

QT implementation mimics 2017 and purely focuses on logistics

A focus on “deliberate/consistent/methodical” policy action as base case when asked about 75bps but not entirely dismissive (see Mester below)

DOVISH

No change to statement: “anticipates that ongoing increases in the target range will be appropriate.”

QT June start, 60bn UST/35bn MBS phase in period of > 3months

Global risks a fixture of the presser w.r.t. risk to downshift in growth

Powell rejects the idea that he would surprise with 75bps (see Bostic below

* * *

Fedspeak on the use of 75bps:

Q: What about a 75 basis point hike which is something that’s been mentioned lately is that something you’d consider?

Mester: As we always say at the fed we consider everything. My own view is we don’t need to go there at this point and I’d rather be more deliberative and more intentional about what we’re planning to do and I see being on the path we’re on now, I would support at this point, given where the economy is, a 50 basis point rise in May and a few more to get to that 2.5% level by the end of the year and I think that’s a better path I mean doing one outsize, a one-off outsized move in the funds rate doesn’t really appear to me to be the right way to go. I would rather be more deliberative and more consistent in bringing up the funds rate and signalling that that’s what the path we’re on and then when we get to that neutral rate where policy goes after that is going to really depend on how that policy has affected the economy as well as these other factors we know that fiscal policy is going to be waning this year, the effects of the pandemic results, but we don’t know how that’s going to look. And so let’s be on this methodical rather than overly aggressive path and then see how policy transmits to the economy and see how the economy evolves. It’s always good to remember that monetary policy transmits to the economy, the expectations and movements in financial markets so that’s why I kind of favor this methodical approach rather than a shock of a 75 basis point I don’t think it’s needed for what we’re trying to do with our policy.

Asked about hiking by a larger amount, Daly says “the tactics about is it 50 (basis points), is it 25, is it 75, those are things I’ll deliberate with my colleagues. But my own starting point is we don’t want to go so quickly or so abruptly that we surprise Americans and make them have to adjust quickly”

Q: Would you consider 75bp hikes?

Bostic: “I’ve been saying for months now that any action is actually possible although it’s not really on my on my radar right now. But I think what’s going to happen is that you’re going to see a steady march of our policy, assuming that the economy evolves the way it has the last several months. As we take each step, it will give us an opportunity to observe and adapt our policy based on what we see. Even just now, if you look at what’s happening to real wages real personal income, real personal incomes have grown at a negative rate, decreased in last six or seven months and real wages are in retreat. If that continues, there is a real case to be made that demand is going to slow down in ways that our policies will accelerate but it will allow us to not have to push as hard. But all of that is conjecture at this point we’re going to have to watch and see what happens and then evolve as are we as we learn the reality. “

On 75bps:

Bullard: “Yeah, more than fifty basis points is not my base case at this point. I would point out that the 1994 cycle, where we raised the policy rate 300 basis points in a year—first of all, that one was successful and did set up the U.S. economy for a stellar second half of the 1990s, one of the best periods in U.S. macroeconomic history. So it was successful. And in that cycle, there was a seventy-five basis point increase at one point. So I wouldn’t rule it out, but it’s not my base case here.”

Q: more than one 50bps?

Waller: “The data has come in exactly to support that type of policy action if the committee chooses to do so. It gives us the basis for doing it. I’ve said before I prefer a front-loading approach so a 50bp hike in May would be consistent with that and possibly more in June and July”

* * *

We’ll conclude with a rather cynical view, commenting from the latest Bear Traps Report from Larry McDonald who best summarized what’s at stake today:

The Fed went to 50BN a month in September of 2018 and had to stop five minutes later in December this was after promising Wall St economists they were on Auto pilot all the way up to a 2T reduction. Now, they are going to give it a try at 90B a month in May with back to back 50 bp hikes? Who are they kidding?

It’s the worst start to a year for stocks in decades, consumer savings is down to the bone, GDP prints negative, and the Fed is going to kick off a record tightening cycle? It´s all a show. With conviction we see a near term top in the US dollar and another leg up for hard assets, value vs growth and emerging markets.

Tyler Durden

Wed, 05/04/2022 – 12:45

Please follow and like us: