Charting America's Single Mothers By Ethnicity There are 7.3 million single mothers in the U.S., as well as 1.9 million single fathers. Single parents...

Read More

Wall Street’s Biggest Bear Sees Much More Pain, S&P Dropping As Low As 3,350

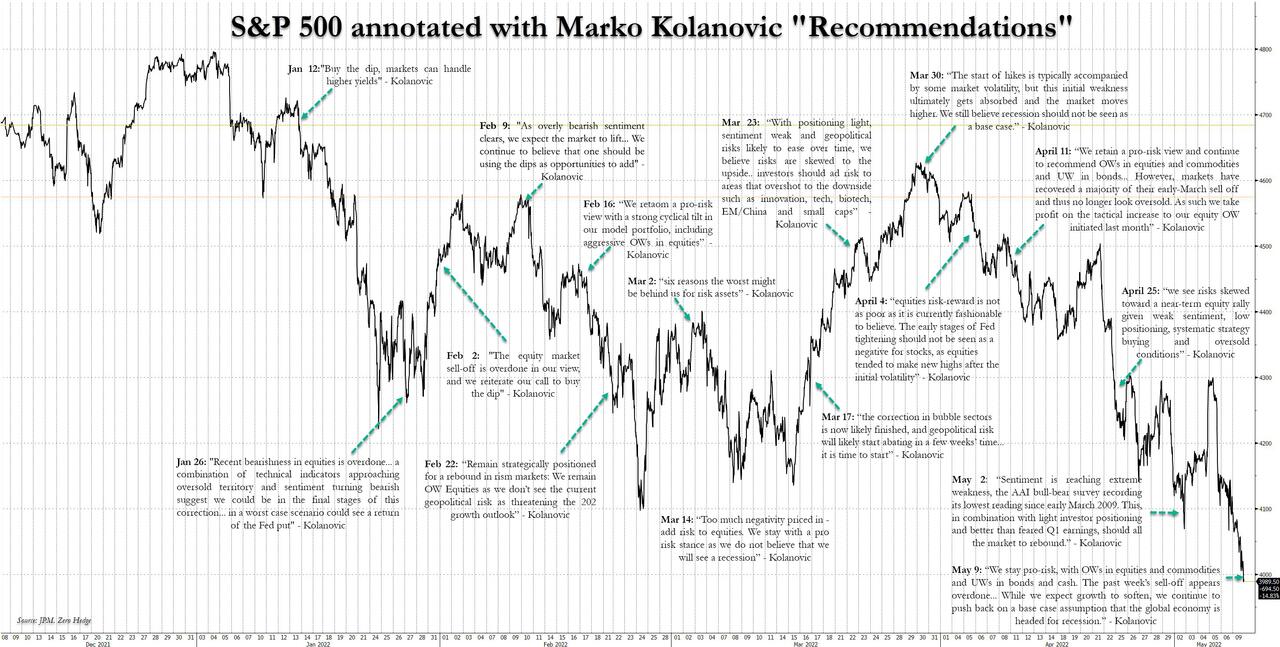

On the surface there isn’t a big difference between Morgan Stanley’s Michael Wilson and JPMorgan Marko Kolanovic: both of them are best known for fiercely sticking to their financial view and week-after-week hammering their market position, come rain or shine. The only difference, of course, is that while Marko has been wrong for all of 2022 – a fact which hasn’t bothered him one bit and this week he urged what few clients he has left to BTFD for the 19th consecutive week even as the S&P tumbled 1000 points below his year-end price target of 4,900…

{kind=link}

… Wilson has been bearish all along, and right. And just as Kolanovic refuses to stop digging the hole he is in, and keeps on repeating that any minute now the ramp will arrive and stocks will merrily return to their all time highs, so Wilson keeps pouring salt into the wounds of bulls – who suddenly find themselves alone and without the Fed’s tender, loving POMOing care – and in his latest note, a Mid-Year Outlook Forecast published today (available to pro subscribers in the usual place) he warns that not only is the rout in stocks not over (despite the S&P just 50 points away from his base-case year-end target of 3,900) but he sees much more downside in a worst case scenario amid mounting concerns of slowing growth.

Warning that the US equity market “is not priced for this slowdown in growth from current levels” and in fact, based on Wilson’s fair value framework, “the S&P 500 is still mispriced for the current growth environment”, the strategist leverages the relationship of PMIs versus equity risk premium over time to project fair value ERP based on the current level of the US ISM Composite PMI. Based on this approach, fair value ERP is 330bp. Applying today’s 10-year yield to Wilson’s fair value risk premium, indicates a forward multiple of ~16x and an S&P 500 price level of 3,700-3,800.

{kind=link}

Weaving that tactical setup in Morgan Staney’s forward 12-month price target of 3,900 implies that the market is expected to overshoot his target to the downside in the near term before working back toward 3,900 next spring (by reference, JPMorgan still expects the S&P to close the year at 4,900).

Some more bearish observations from Wilson:

We’re in the midst of a hotter but shorter cycle in the US. We first made this case in March of last year, arguing that this cycle was likely to progress quicker than the prior four given the velocity of the growth rebound following the Covid recession, the return of inflation after a 40-year absence, and a much earlier-than-expected shift to more hawkish monetary policy. Fast forward to today, and that’s what appears to be happening—earnings have accelerated past prior cycle peaks historically quickly and are now starting to decelerate from a growth rate perspective, inflation is at a multi-decade high, and the Fed has hiked twice just two years into the cycle.

The key implication here is that the early-to-mid-cycle benefits of positive operating leverage are behind us, and earnings growth is likely to decelerate, driven by margin compression and slowing top-line growth. This dynamic is confirmed by output from our leading earnings model and the recent downward pressure we have seen in earnings revisions breadth. Coupled with decelerating PMIs, this downdraft in earnings growth we expect into next year gives us high conviction that our ‘ice’ scenario has arrived and it’s here to stay for even longer than we envisioned going into this year.

{kind=link}

Why can Wilson’s ‘ice’ scenario persist in the context of a hotter but shorter cycle? Four reasons:

The Russia/Ukraine conflict has exacerbated inflation pressures particularly for energy and food; these cost pressures continue to weigh on already depressed consumer sentiment.

Labor and input cost pressures remain sticky and continue to pose a risk to corporate profit margins.

Tighter monetary policy is now having an economic impact, particularly within the housing market, where affordability and mortgage costs are affecting households.

We’re starting to see signs that excess inventory is building in consumer goods; it’s happened more slowly than anticipated, but that means pricing/discounting risk for impacted companies can linger for several quarters.

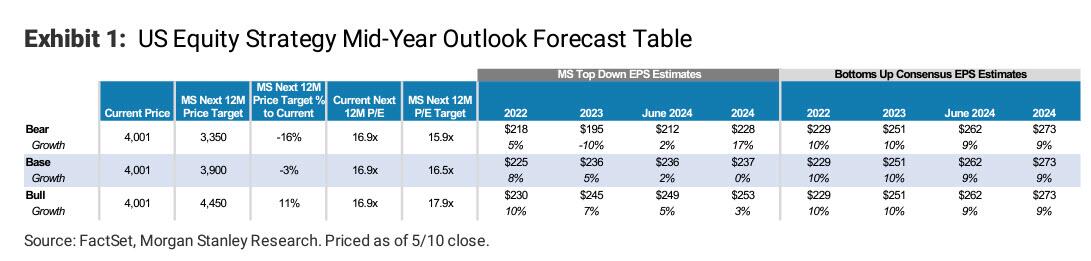

Finally, here is a breakdown of Wilson’s three price target cases for Q2 2023:

{kind=link}

Base Case Price Target for 2Q23: 3,900

In our 3,900 base case, the market puts a 16.5x P/E multiple on forward (June 2024) EPS of $236. We expect the market multiple to de-rate further from current levels over the next 12 months driven by a higher equity risk premium (~325 bps) as earnings, economic, policy and geopolitical uncertainty remain high. While the multiple compression we embed in our base case is fairly modest given the recent drawdown we have experienced in equities, we think the risk is elevated that the market multiple overshoots our base case to the downside in the near term (see Weekly Warm-Up: That Escalated Quickly As News Always Follows Stocks). On the earnings front, we take down our estimates as cost pressures continue to ramp up, top line growth slows and output from our leading earnings model points to a further deceleration in EPS growth. Our earnings estimates are now well below consensus out to 2024. Specifically, we see 8% growth in ’22 (consensus is at 10%), 5% growth in ’23 (consensus is at 10%) and 0% growth in ’24 (consensus is at 9%). In short, the over-earning that took place post the covid recession is worked off as demand slows and cost pressures eat into margins. In the absence of a recession (our economists’ base case view), this dynamic happens less abruptly at the overall index level, but we continue to believe it may feel like a recession for certain areas of the equity market over the next twelve months (specifically those areas tied to the consumer goods and technology overconsumption that transpired in 2H ’20 and ’21). Bottom line: ‘fire’ AND ‘ice’ persist as the Fed continues to tighten policy into a slowing growth environment. Expect decelerating earnings growth, a lower multiple and elevated volatility. An overshoot to the downside of our next twelve month multiple and price targets is likely tactically as the market discounts (in advance) the consolidation in earnings expectations we expect to transpire over the coming months.

Bull Case Price Target for 2Q23: 4,450

In our 4,450 bull case, the market puts a 17.9x P/E multiple on forward (June 2024) EPS of $249. A soft landing is achieved in our bull case. The Fed’s hawkish path is not a risk to the US growth backdrop, consumer confidence rebounds as inflation fades, cost pressures ease along with inflation as supply chains reopen in an orderly manner, corporates maintain pricing power, and any excess inventory build in consumer goods is absorbed by household demand. As noted in the Global Strategy Mid-Year Outlook, this scenario could also involve changes to China’s covid policy and a more positive geopolitical situation in Europe. Amid this backdrop, multiples expand to 17.9x, and the equity risk premium remains around post-GFC lows (~280 bps). On the earnings front, growth is modest but still positive out to 2024 as margin pressures are less significant than in our base case. Bottom line: earnings growth slows but is still positive, cost pressures ease as inflation is curbed, consumer confidence rebounds, and excess inventory in consumer goods is absorbed—a soft landing where multiples have room to expand.

Bear Case Price Target for 2Q23: 3,350

In our 3,350 bear case, the market puts a 15.9x P/E multiple on forward (June 2024) EPS of $212. This scenario assumes a recession. We have earnings growth decelerating in 2022 and then outright negative in 2023 (-10%) from a calendar year standpoint. We then see 2024 EPS growth rebounding off of recession comps, finishing the year +17%. In this scenario, margin contraction is more severe in 2022 and 2023, and nominal top line growth nearly contracts on a year-over-year basis by 2023, only kept modestly positive by inflation. Bottom line: sticky input/labor cost inflation drives sustained margin pressure. Payback in demand is a dominant theme, leading to a broad deceleration in sales growth. That combination takes EPS growth negative in 2023. At the same time, stickier inflation keeps the Fed on a hawkish path despite decelerating growth and tightening financial conditions.

Wilson’s call is in sharp contrast to not only Marko Kolanovic who absurdly keeps telling clients to just keep buying stocks into the abyss, but even more respected strategists including Peter Oppenheimer at Goldman Sachs who said on Tuesday that the powerful selloff in stocks in the past weeks had created buying opportunities, with headwinds such as inflation and hawkish central banks already priced in. So far Wilson (and BofA’s Hartnett) is right and all of his bullish competitors have been dead wrong.

There is more in the full Morgan Stanley note available to professional subs.

Tyler Durden

Wed, 05/11/2022 – 15:31

Please follow and like us: