Trump Did It: Executives & Administrators Are Increasingly Using TDI To Fight DEI Authored by Jonathan Turley, “Trump made me...

Read More

CPI’s 15 Minutes Of Fame…

Authored by Peter Tchir via AcademySecurities.com,

Everyone is waiting for Tuesday’s CPI data. We will get officially told what inflation was in August. It is unlikely that it will reflect what we see and feel every day. It doesn’t tell us anything about where September will be (actually, that is not true, as some of the data will be so off, that it will have to get fixed in next month’s report, and some is just stale by its nature (housing)).

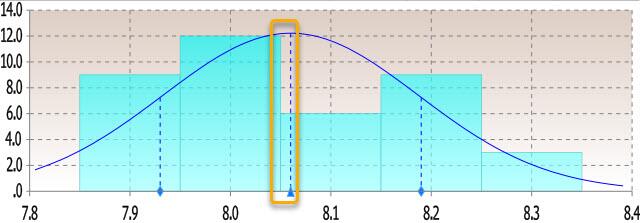

There are 39 estimates on Bloomberg (compared to 72 estimates for this month’s NFP data). The range is incredibly narrow (7.9% to 8.3% for YOY).

{kind=link}

In theory, it will set the framework for the Fed’s rate decision and press conference on September 21st (the press conference has become as important, if not more important for markets, than the hikes themselves).

The reality is that CPI, away from quirks in how it is calculated (the all-important housing component might be the quirkiest off the quirky, but heuristic adjustments, how prices are measured, etc.) all impact the number that we will be given, but don’t really impact the inflation we have. And again, it doesn’t tell us much about the future of inflation.

As we sent out on Friday, the market has concluded that both the ECB and even the Fed, despite their protestations otherwise, are both being viewed as data dependent.

I cannot see any scenario, where the market doesn’t decide that CPI is heading the right direction and that October will be lower than September and so on and so forth (so many commodity futures contracts that I checked out are all lower forward than spot).

That combination should allow markets to continue to enjoy the strength that they saw towards the end of last week.

What Really Matters

I continue to see 4 Main Themes for September:

Russia and European Energy. We’ve seen the U.K. start to transfer some of the energy problems facing consumers and companies onto the government’s balance sheet. Lagarde indicated other countries will do something similar. I’m not sure we’ve seen peak problems in Europe yet on the energy front, but this is a good development. With so much bad being priced in, we could see a nice short squeeze in European credit and equities.

Inventories and New Orders. This is the crux of my concern and why we are as likely to be talking about deflation as inflation by year-end. The data will come out in dribs and drabs, but will be a key determinant of future inflation.

Housing, Real Estate and Autos. Even with yields stabilizing (or not hitting new highs), we are likely only starting to see the impact of higher yields on these products. The mortgage market is key, but I’m hearing rumbling that QT will shift away from selling mortgages, which would bring mortgage spreads down dramatically, which would help support housing. I think the worst is behind us on rates, and for the moment that is helping risk assets, but that “bad news is good news” trade seems tenuous at best.

Wealth Effect. Canada lost jobs for the third month in a row while we pump out great jobs reports (if not in the household survey, the establishment survey (until they get revised down 2 months later)). The lost wealth in stocks, bonds and crypto is real and still significant. The reduced ability to spend by companies now focused on cash flow is real. Jobs have been good (with the prior caveats), but I remain concerned here.

While CPI has all of our attention, as does the Fed meeting, how the four things that I think matter the most, develop, will be key.

Bottom Line

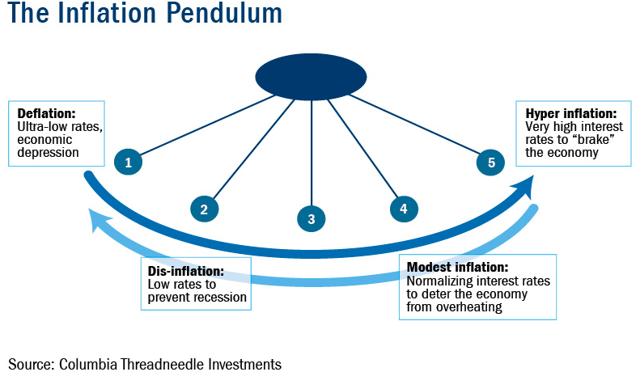

Enjoy the easing of inflation for now. But as I mentioned in a report earlier this summer, a pendulum swinging back, will be at the bottom at one point, but it won’t stop there (I “borrowed” that analogy from the radio, but think it is compelling).

{kind=link}

So, at the moment, the pendulum will look like inflation and monetary policy are in a good place, but I expect that to keep swinging and we will see it has gone too far, but that won’t be apparent until we get CPI and Fed speculation this week!

Never Forget!

Tyler Durden

Mon, 09/12/2022 – 07:20

Please follow and like us: