Trump Did It: Executives & Administrators Are Increasingly Using TDI To Fight DEI Authored by Jonathan Turley, “Trump made me...

Read More

Nomura Fears Market “Tsunami” From Fed “Butterfly Flapping Its Wings”

Everyone and their pet rabbit is heading into today’s FOMC meeting long the dollar, short bonds, and underweight/low-nets to stocks (with extreme negative gamma from hedges).

{kind=link}

That combination has Nomura’s Charlie McElligott worrying about what is essentially a “butterfly flapping its wings” moment, where simple monetization / closing / or profit-taking then risks a larger unstable reversal, turning into a “un-economical” market impulse which is not related to any fundamental change in macro stance.

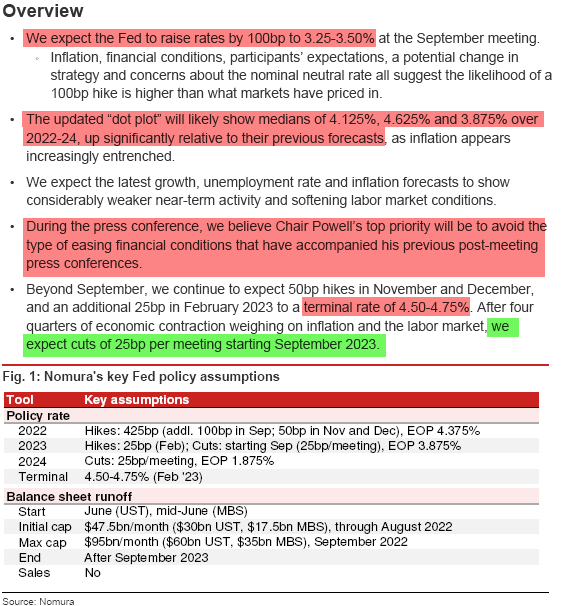

Despite Nomura’s “hawkish” out-of-consensus house view that The Fed will hike 100bps today…

{kind=link}

…McElligott is not fearful of “hawkish / FCI tightening” trend extension with Fed (frankly that should be GOOD for consensus positioning), nor is he overly concerned by some perceived “fundamental shift” in hawkish messaging, or the market’s perception of “where we are” in the tightening cycle, just as US Terminal Rate projections just hit fresh highs in recent days.

Instead then, he writes:

…my worries are simply about a “butterfly flapping its wings” market moment, where the slightest bit of “monetization” of “working” trades could build into an tsunami of “reversal” price-movement on “stop-outs,” and frankly with little-to-no fundamental rationale besides “POSITIONING”.

The crowded “FCI tightening” macro trend trades of 2022—Long Dollar, Short Bonds / STIRs, Short Equities—are, in a vacuum, from a pure “asymmetric positioning” perspective, at greatest risk of reversal today on any sort of post FOMC market inflection, where covering and / or profit-taking could then become a stampede of unwind

The “clearing” of this week’s particularly acute Central Bank “hawkish impulse” event-risk, where 9 central banks globally have tightened policy rates over a collective 500bps in a 3 day period, could in-fact stand as the largest—and probably most “counter-intuitive”—catalyst for said reversal in trend trades, particularly risking an Equities squeeze for “un-economical” reasons.

His concerns on Equities “reversal / squeeze higher” dynamics are in-particular due to Options Positioning dynamics… where previously highlighted in recent notes “Low Nets / low %ile Rank Exposure / Outright “Shorts” / Extreme Low L/S, Macro and Mutual Fund “Performance Beta to S&P” becomes extremely susceptible to the hedging dynamics within the Vol universe.

This is due of course to the current “Short Gamma vs Spot” dynamic with Dealer positioning across US Equities Index / ETF Options, but particularly due to the extremely acute “Negative $Delta” associated with said Options…

{kind=link}

…which continues to act as “fodder for a squeeze” in the case of a Spot rally, ESPECIALLY with clients continuing to load into extremely short-dated (0-5DTE) Downside / Puts that are hyper sensitive and which would see bulk closing-out if stocks were to squeeze meaningfully higher, creating “POSITIVE $DELTA” flows as Dealers cover their short hedges in futures.

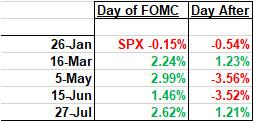

Finally, historical bias tends to support a large “day of” movement, followed by generally outlier instances of “next day” unwind (although last meeting saw that trend broken, as the short-squeeze accelerated further):

{kind=link}

…and then McElligott warns, there is the chance that any rally in Spot for “positioning” or “un-economical” reasons would then risk “activating” the Dealer “LONG Gamma” up at the 4005 strike for month-end from the oft-discussed “Put Spread Collar,” risking strong “gravitational pull” ~ 4000 of around $1.75B.

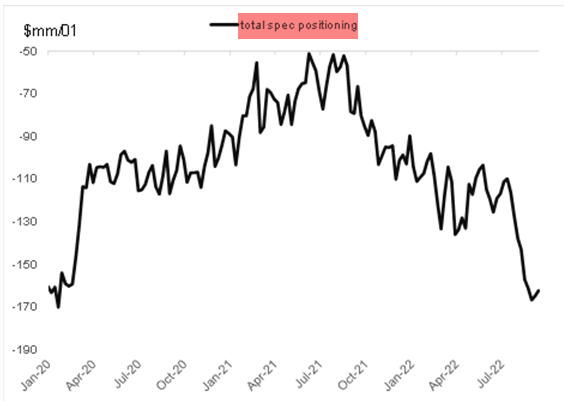

And within Rates / Bonds, there is potential for similar “non-fundamental” squeeze potential, just based-upon the magnitude of the “Consensus Short / Underweight / Low Historical Exposure,” particularly across LEVERAGED strategy types:

{kind=link}

In other words: brace! (or cut nets).

Tyler Durden

Wed, 09/21/2022 – 13:00

Please follow and like us: