Trump Did It: Executives & Administrators Are Increasingly Using TDI To Fight DEI Authored by Jonathan Turley, “Trump made me...

Read More

The Fed Is Wrong Again: Core Inflation Rapidly Rolling Over And Will Drop To 3% By Q1

The Fed was dead wrong for the past decade in perpetuating QE long after the economic crisis had passed, but especially in 2020 and 2021 when it saw nothing but transitory inflation, and refused to step in an contain soaring prices which we are seeing today everywhere in action. And the Fed is also dead wrong now in its crusade to crush inflation – as it confirmed today when it hiked 75bps and telegraphed another 145bps of rate hikes – even if it means a grave recession.

Why is the Fed wrong again? Because besides sliding commodity prices (which will very likely soar in the very near future, especially once winter arrives in Europe and once Biden’s drain of the SPR is over), the bulk of core CPI components – and certainly some of the biggest drivers such as shelter, cars and airfares are rolling over fast.

That’s according to a new report by JPM’s Phoebe White (full note available to pro subs here), who writes that she forecasts a material softening in inflation across all of the components that have been the largest contributors of core inflation over the past year—not only vehicle prices, but rents, medical care services, and airfares as well—and last week’s hot CPI report does not change this view.

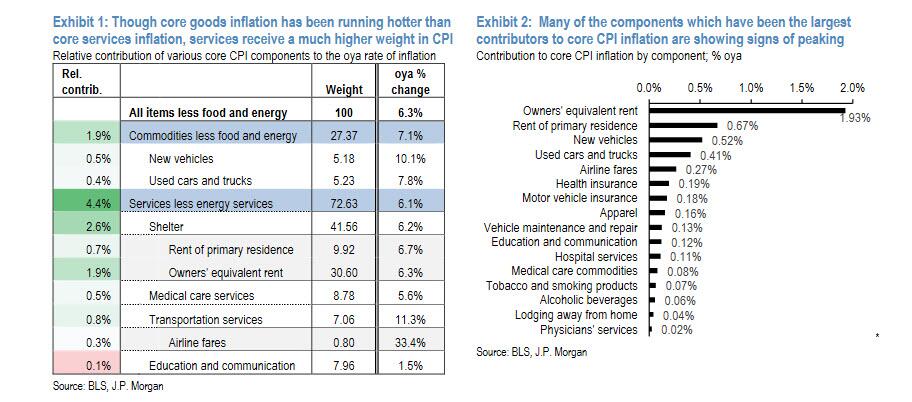

At a high level, we have seen a continued rotation in the composition of core inflation over recent months, with core services inflation accelerating from 3.7% Y/Y as of December 2021 to 6.1% as of August 2022, while core goods inflation has decelerated from 10.7% to 7.1%. Notably, even while core goods inflation continues to run hotter than core services inflation, services receive nearly triple the weight in the calculation of the core index, with the rent components alone comprising more than 40% of the basket (Exhibit 1). Thus, it is clear to see why rent inflation, which has accelerated above 6% Y/Y in recent months, is the largest contributor to core CPI inflation as of the August report: Exhibit 2 shows that the two rent measures, owners’ equivalent rent and rent of primary residence, account for 1.9%-pts and 0.7%-pts, respectively.

{kind=link}

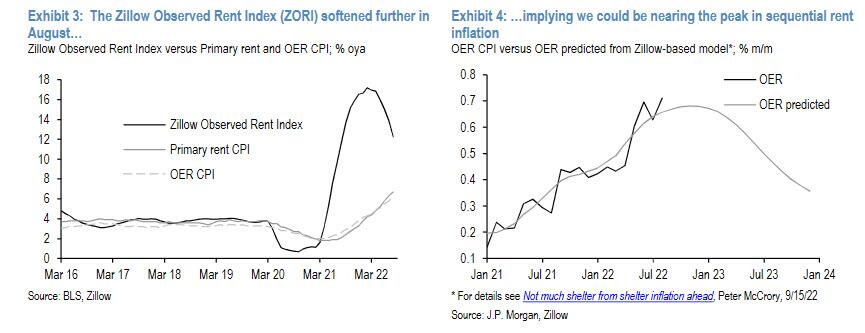

Let’s drill down into the data, starting start with rent inflation – which is the largest contributor to Core Inflation – and which the JPM analyst expects to peak in the next few months and roll over. Why? Take the Zillow Observed Rent Index which like the Apartment list price index (which we have discussed countless times especially when it was soaring higher), tends to lead the CPI rent measures, and this index has been softening recently.

And while JPM expects shelter inflation to break above 7% Y/Y by early next year – due to its several month delay from real-world prices – the bank also expects the pace of monthly gains to peak within the next few months. The rate of increases in the Zillow Observed Rent Index, which measures asking rents on new leases, peaked above 17% in February, but has softened to 12%

oya as of August—a notable softening, albeit still elevated versus the ~4% average pace observed prior to the pandemic. Unlike the Zillow data, the rent components in CPI track average rents across both new and existing leases. Thus fluctuations in the Zillow index slowly pass-through to official measures as the stock of leases begins to resemble the recent flow of new leases, with each percentage-point increase in the Zillow rent index preceding a 0.6%-pt cumulative increase in shelter CPI .

{kind=link}

To be sure, one complicating dynamic that we have been highlighting is the fact that tighter monetary policy could temporarily exacerbate rental inflationary pressure, as high mortgage rates discourage home-buying. Indeed, now that no new home buyer reliant on a mortgage can possibly afford a house, they will likely have no choice but to find a rental. On the other hand, there is a limit to how high rents can go simply as a function of disposable income: outside of the top income cohort, JPM finds that rent affordability is already stretched, implying it will be difficult for rent inflation to sustain rates much above the pace of wage growth. And once neither housing nor rent is affordable, well then it becomes a political issue and Democrats will scream bloody murder – as Liz Warren already did today – and will demand Powell to start cutting rates.

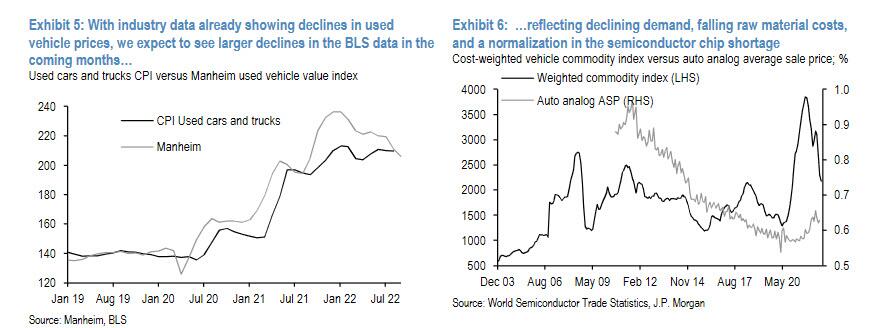

Away from rents, new and used vehicles have had the next largest contributions to core CPI. And with demand softening, supply constraints easing, and raw material costs falling, JPM thinks declines in used vehicle prices are on the near-term horizon. Declines in new vehicle prices are likely to follow in 2023. In fact, the Manheim Used Vehicle Value Index, which measures the prices dealerships pay for used cars at auctions, has declined since its peak in January, with the index falling 4% in August alone, and another 2.3% over the first half of September.

When will this slowdown appear in official data: as chart 5 illustrates, the pass-through from the Mannheim index to the BLS data exhibits a 1-3 month lag, making it somewhat difficult to forecast the precise timing of inflections in the used vehicle CPI. Looking ahead, JPM expects the trend of falling used vehicle prices to continue over coming months: Chart 6 shows that the J.P Morgan Automotive Commodities Index is now down 35%, reflecting the cost-weighted average price of the commodities used to manufacture a vehicle. Used vehicle prices tend to be more sensitive to raw commodity costs compared with new vehicles, given that scrap value reflects a greater share of the overall price of a used vehicle.

{kind=link}

The component with the next largest contributions to core CPI inflation is airline fares which is one of the more highly volatile categories of inflation. The still-high rate of airfare inflation on a year-ago basis reflects the surge observed through the spring alongside rising jet fuel prices, but this component has fallen by more than 14% since its peak in May, with prices likely to be somewhat more stable going forward.

Finally, the recent surge in health insurance inflation likely reflects, at least in part, the drop in insurance claims over a year ago, given the “retained earnings” methodology that BLS uses to calculate this component. Some utilization metrics are now tracking in line with pre-pandemic levels

Overall, when taking a deeper look at the largest contributors to core CPI inflation over the past year, JPMorgan sees clear evidence that core inflation is peaking and is likely to moderate fairly quickly on a sequential basis over the near term, falling from 6.5% in the three months through August, to about a 3.5% SAAR pace in 1Q 23 and just 3.1% in 2Q23, or essentially in line with the Fed’ target.

To be sure, the longer it takes for these dynamics to play out, the greater the risks that high inflation could become more ingrained. However, what is even more relevant is that the latest hawkish rate hike by the Fed – which guarantees that the Fed overshoots, driving a more material weakening in demand and triggering a recession — will certainly lead to even softer inflation. In other words, if the Fed halts its tightening campaign here, not only will core prices drop to where the Fed wants them, but a recession may even be averted. However, if Powell continues blindingly to hike, a crushing recession is virtually guaranteed. And since the Fed is always wrong about everything, the worst case scenario is now in play.

Much more in the full report available to pro subs in the usual place.

Tyler Durden

Wed, 09/21/2022 – 20:00

Please follow and like us: