A Third Of Americans Worry About Manipulated News Almost half of the people surveyed in the United States as part of a...

Read More

2 Trillion Reasons Why Today’s Market Has “Increased Potential For Instability”

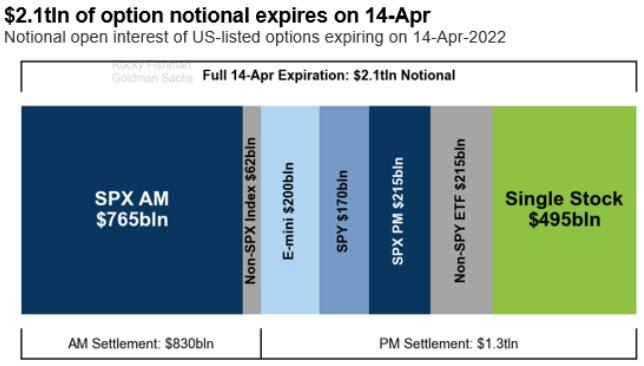

The holiday shortened week means that traders face an early options expiration today – in an already illiquid market environment – with over $2 trillion notional set to expire…

{kind=link}

Goldman’s derivative guru, Rocky Fishman, estimates that roughly $495 billion in single-stock derivatives are set to expire, with another $980 billion of S&P 500-linked contracts, and an additional $170 billion in options tied to the SPY ETF expiring into the close.

Aside from the timing and size of the options expiration, Steve Sosnick, chief strategist at Interactive Brokers, notes that there are other “wrinkles” arising due to the proximity of tax day and the start of earnings season, “both of which we’re getting now.”

The last few months have seen index options volumes resurgent (macro overlays and hedges) while the more speculative FOMO single-stock options volumes have lagged…

{kind=link}

“This is likely due to more of a focus on the macro environment and more hedging,” said Chris Murphy, co-head of derivatives strategy at Susquehanna. And as single-stock options volume has fallen, the single-stock put/call ratio has risen off multi-month lows as cautious traders reposition from the FOMO days of Stimmies and Stonks.

{kind=link}

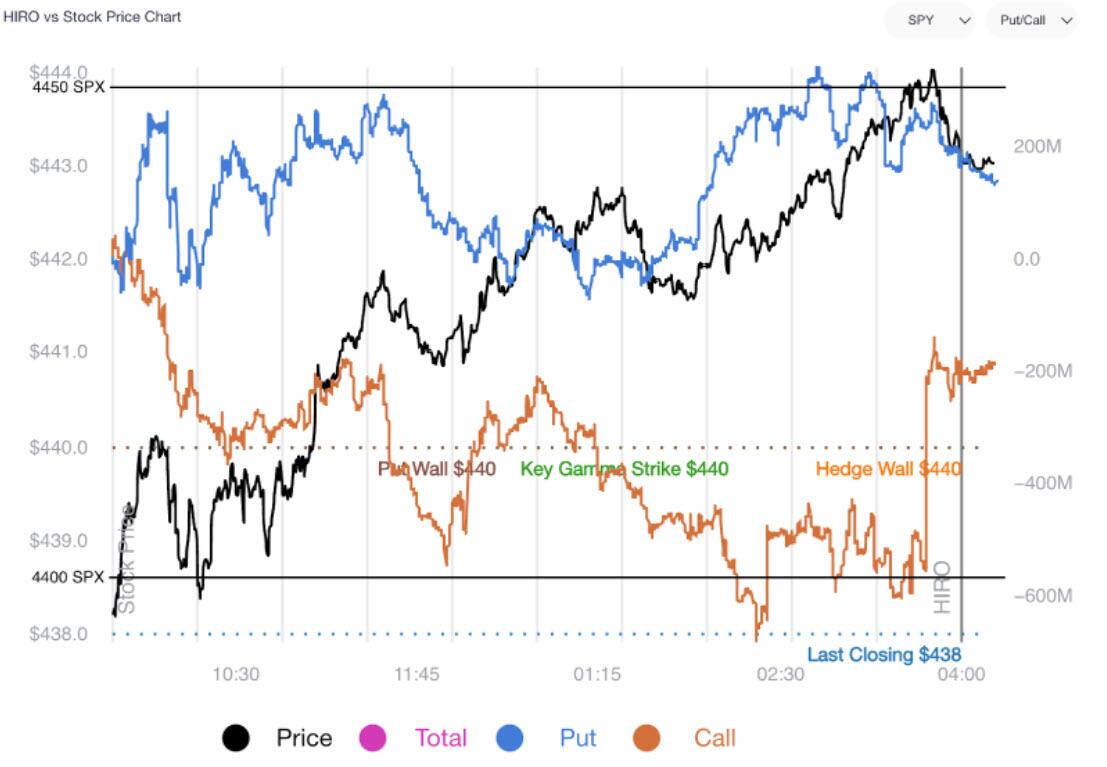

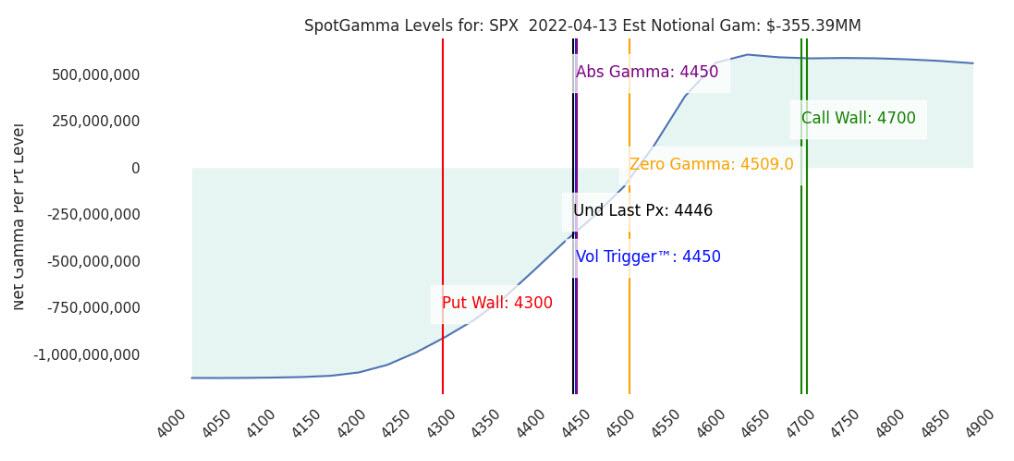

All of which sets the stage for today’s fun and games as SpotGamma warns that there is increased potential for instability so long as participants maintain SPX prices below the 4,450.00 Volatility Trigger.

{kind=link}

In such a case, dealer hedging flows would take from market liquidity (buy strength and sell weakness), potentially exacerbating underlying movement.

However, there is some tendency for volatility-selling into the extended weekend, which we saw yesterday providing supportive flows (much of which may have actually bolstered today’s rally to perfectly tag SPX 4450 into the close – even as the actual SPY options trading was neutral-to-negative)…

{kind=link}

But SpotGamma warns, if the Put Wall rolls lower and the SPX starts to slip, caution…

{kind=link}

… You may be looking at a market that has more room to the downside.

If metrics like the implied volatility term structure invert (shorter-dated contracts are higher than longer-dated contracts), hedging flows with respect to changes in volatility (vanna) will only worsen the existing negative gamma-hedging component.

Currently, SpotGamma sees roughly 40% of total SPX/SPY/QQQ Gamma expiring by today’s close, and roughly 50% of single stocks having their largest gamma position expiring too. Below they discuss the hedging flows tied to April OPEX with options expert Imran Lakha about

Tyler Durden

Thu, 04/14/2022 – 07:00

Please follow and like us: